[This is one of the finalists in the 2026 book review contest, written by an ACX reader who will remain anonymous until after voting is done. I’ll be posting about one of these a week for several months. When you’ve read them all, I’ll ask you to vote for a favorite, so remember which ones you liked]

Part 1.

The Book of Abraham opens with this paragraph:

“A Translation of some ancient Records that have fallen into our hands from the catacombs of Egypt. The writings of Abraham while he was in Egypt, called the Book of Abraham, written by his own hand, upon papyrus.”

As you can read, The Book of Abraham was written by grand patriarch Abraham upon papyrus while he was in Egypt. Someone managed to get their hands on these papyri and then subsequently translated them into English. This is of profound historical importance if true, because otherwise there is no direct evidence that Abraham existed as a specific historical individual.

Who got their hands on these writings? The Mormons. More specifically their founding prophet Joseph Smith who a few years previously translated some other Egyptian writings into the Book of Mormon. The Book of Abraham is not that well-known in comparison, but it’s considered canonical scripture in the Mormon church.

The Abraham papyri were obtained by the Mormons in 1835 from a traveling antiques exhibitor, five years after the formal establishment of the Mormon church. A time at which it was experiencing a surge of new converts, with the membership doubling from 1834 to 1835.

During these times there was an enormous fascination with the ancient world in the US and Europe, particularly ancient Egypt. After Napoleon’s Egyptian campaign in 1801, Mummies were exported by the thousands into Europe and the US, making them surprisingly cheap and common. People would pay good money to see mummies or ancient artifacts being toured around.

It even became fashionable among the wealthy to host “mummy unwrapping parties” where they would buy a mummy, then invite all their friends to a party where the main entertainment would be watching a showman slowly remove bandages from the mummy while loudly dramatizing the whole affair. Hoping to uncover some cool trinkets or artifacts that would make the guests gawk.

Which sounds deranged today, but isn’t really: status signals are somewhat arbitrary. Remember MTV’s “My Super Sweet 16,” where the birthday girl has a meltdown because her Porsche arrived in the wrong color? If modern Sally is allowed a freakout, so is Victorian Sally:

Among other brave endeavors, they would ground the mummies into a fine powder and consume it as medicine even though cannibalism was generally considered to be gravely sinful. Mummy powder was also used as an aphrodisiac. Reading all this, I couldn’t help but reflect a bit on that famous Percy Shelley poem:

I met a traveller from an antique land,

Who said: “Two vast and trunkless legs of stone

Stand in the desert. . . . Near them, on the sand,

Half sunk a shattered visage lies, whose frown,

And wrinkled lip, and sneer of cold command,

Tell that its sculptor well those passions read

Which yet survive, stamped on these lifeless things,

The hand that mocked them, and the heart that fed:

And on the pedestal, these words appear:

My name is Ozymandias, king of kings:

Look on my works, ye mighty, and despair!”

Nothing beside remains. Round the decay

Of that colossal wreck, boundless and bare

The lone and level sands stretch far away.

One day you’re Ozymandias, king of kings, the next you’re smeared on some guy’s dick to help get him hard. What to do.

A factor fueling the fascination with ancient Egypt was that a bunch of Egyptian papyri were floating around, but nobody in the US knew how to translate them. A mystery! The Rosetta Stone had just recently been deciphered in Europe, but the knowledge had not yet propagated to the Americas. So when traveling antiques exhibitor Michael Chandler was touring around his collection of mummies and papyri scrolls, he frequently asked around for people who could translate what was written on them.

At some point Chandler heard word of a man in Kirtland, Ohio, who claimed to have the spiritual gift to translate ancient languages: Joseph Smith, who had recently published the Book of Mormon after translating it from Egyptian inscribed on ancient golden plates. Intrigued (and likely seeing a business opportunity) Chandler brought his exhibition to Kirtland in July 1835.

Chandler presented the papyri scrolls to Joseph Smith. Joseph examined the papyri and, according to his own account, was given a revelation about their contents. Joseph announced to his followers that he had identified the writings on the scrolls as the literal writings of the ancient biblical patriarchs:

“I commenced the translation of some of the characters or hieroglyphics, and much to our joy found that one of the rolls contained the writings of Abraham, another the writings of Joseph of Egypt...” (History of the Church, 2:236).

The Church (which had just started and was not rich at the time) pooled together their resources to buy Chandler’s entire collection, including the papyrus scrolls. During the following years Joseph would study the scrolls and dictate his translation to his scribes.

Interlude 1.

Joseph Smith would put the seer stone into a hat, and put his face in the hat, drawing it closely around his face to exclude the light; and in the darkness the spiritual light would shine. A piece of something resembling parchment would appear, and on that appeared the writing. One character at a time would appear, and under it was the interpretation in English.

The preceding paragraph is a quote from one of Joseph Smith’s scribes describing the translation process that produced The Book of Mormon (not The Book of Abraham).

In 1827 (8 years before the Abraham papyri), Joseph dug up golden plates buried in the ground near his home in New York after being directed there by an Angel. These golden plates contained inscriptions of a highly information dense version of ancient Egyptian. With the help of God he translated these inscriptions into English, revealing a huge biblical plot twist: JESUS WAS IN AMERICA.

Shortly after Jesus’ resurrection, he traveled to the Americas to bless the people living there at the time, who weren’t Native Indians, they were Israelites who had voyaged to the US in 600 B.C using something resembling a wooden submarine. Shortly after, God would punish some of the less godly Israelites by transforming them into Native Indians, specifically so that they would not be enticing to the white people, preventing the spread of rotten seed.

After a thousand years of war between the bad Native Indian Israelites and the good white Israelites, the good ones are losing badly and are in the process of being genocided by the Native Indians. One of the last surviving non-Indian Israelites called Mormon manages to gruellingly inscribe the history of all this onto Golden Plates over the course of decades before dying, leaving the last patch of work to his son Moroni, who is now the last survivor of his people. Moroni completes the work (alone) and spends the next few decades (alone) evading capture while personally carrying heavy golden plates from Central America to New York, where he buries them in the ground because he’s been told by God that this is where Joseph Smith will find them a thousand years later and translate them into English.

Anyways, Joseph’s fellow Americans thought the idea that Jesus had been to America was super cool and converts started pouring in. The text that was translated from the Egyptian inscriptions became what we know today as the Book of Mormon and the golden plates disappeared never to be seen again.

That was in 1827. In the following years, Joseph and friends would do some hardcore proselytizing: “Hey, did you know Jesus was in the US? Cool right! Why don’t you join our new church?” I don’t know what their sales pitch was exactly, but whatever it was, it was not bad at all. In April 1830 there were 6 founding members and by December the same year it had grown to around 300. The Book of Mormon is then officially published and the Church is formally organized. Five years later in 1835 they’ve already grown to around 8000 members and in 1837 they had missionaries traveling to England converting tens of thousands in the following years. Not bad numbers for a barely-literate farm boy in just 15 years with no TikTok!

And today there are many millions:

That’s the story from 1827 to 2026. I skipped some details. Compared with other versions of Christianity, Mormonism has many. At least in its early history. This is not because Mormonism is historically or theologically more rich, it’s because Mormonism is far more recent in history.

More recent in history means better technology for logging and documenting and less time for the logs and documents to get lost or so detached from the original context we can’t make unambiguous interpretations of them. The result is that we today have large quantities of very reliable records detailing exact quotes and events pertaining to early Mormon history, many coming directly from Joseph himself. You can even read all the original source texts yourself exactly as Joseph intended them because they’re originally written in English! No need to learn Biblical Hebrew or Classical Arabic like you would need with the Bible or Quran.

I mention this because I’m interested in faith as a potential superpower.

I’m not exactly sure how to describe every component of the faith concept, but it’s got something to do with changing your credence in a proposition without good epistemic reasons. That doesn’t mean there couldn’t be good non-epistemic reasons. Info-hazards are a thing and our emotional system is deeply connected to our belief system. Having certain true beliefs can be the source of constant anxiety and self-doubt.

The coolest one is that you can use faith to solve the coordination problem.

Everyone knows religion functions as an inter-tribal coordination mechanism. We have strong instincts to be nice to our friends and family. We do not have nearly as strong instincts to be nice to the guy in the neighboring village. But, if we both think the God given divine moral law says stealing and lying is bad, then instead we will cooperate and tell the truth. Jesus says:

“You have heard that it was said, ‘Love your neighbor and hate your enemy.’ But I tell you, love your enemies and pray for those who persecute you, that you may be children of your Father in heaven. He causes his sun to rise on the evil and the good, and sends rain on the righteous and the unrighteous. If you love those who love you, what reward will you get? Are not even the tax collectors doing that? And if you greet only your own people, what are you doing more than others? Do not even pagans do that? Be perfect, therefore, as your heavenly Father is perfect.”

Clearly this doesn’t work if you’re constantly encountering people who choose betrayal in the Prisoner’s dilemma. Then you just end up dying. So you have to try and mostly play with people who’re genuinely following similar religious beliefs. This is the famous freeloader problem. Religions solve this by practicing costly rituals. You know I’m a true believer because every Sunday at noon I sacrifice a baby goat and do a tedious 30 minute chant together with all the other true believers. If I do something costly every Sunday at noon, then one might think I’d be more likely to play cooperate in the Prisoner’s dilemma even though playing defect would directly benefit me more.

In theory I could just be paying the costly signals in public as a purely calculated decision because I know it will benefit me long-term. Some people are probably doing that, but in practice I would guess paying the costly signals consistently over time in a believable way is difficult without being a true believer.

We know an outcome of faith is changing your credence in a proposition without good epistemic reason. But what is the mechanism, what are you actually doing in your mind when you try to have faith? Is it like thinking “Jesus is real, Jesus is real, Jesus is real…” in your head over and over?

I just tried it and I think that kind of works to be honest.

Practicing a costly ritual seems like it could also work as a faith-increasing mechanism: You’re using the sunk-cost bias in order to brainwash yourself. Another faith-increasing mechanism is hanging around people who’re also trying to have faith: you’re using your tribal group cohesion instincts in order to brainwash yourself.

In a very literal sense, faith is the opposite of rationalism: you’re knowingly trying to believe something with a greater conviction than what is warranted by the evidence. That’s epistemic rationality though. Instrumental rationality is about achieving The Good. In that sense, faith can be very rational.

Wouldn’t it be nice if all humans on earth could enter into a collective brainwashing ritual where we all ended up thinking playing cooperate in the Prisoner’s dilemma is the correct thing to do?

The Mormons do this really well. They grow up mostly surrounded by other Mormons where they follow strict adherence to various rules and traditions. No drinking, no smoking, no coffee, no sex before marriage. You have to go to Church every Sunday and participate in various other religious and community events. When you get a job you have to pay 10 percent of your salary to the Church. As a teenager you have to work a part-time job so that when you turn 19 you can fund part of your own 2 year mission where you have to become fluent in a second language and travel somewhere random in the world, away from your beloved family, to preach the religion to outsiders who mostly slam doors in your face.

These are all heavy costs. But, in return, the Mormons are very successful. They’re also just better people. Individual Mormon members (ignoring what the Church as an institution gives) consistently give more to charities than almost any other demographic in America. This is on top of the 10% they’re already giving to the Church. They also do more volunteering, even if you only count secular or non-religious community charities. This is on top of all the Mormon-only activities they have to do.

But there’s also no way for Mormonism to *not* demand such heavy costs of its members. If it was a low-demand religion like Christian Protestantism, it would not survive. The reason for this is that Mormonism is only 200 years old.

Part 2.

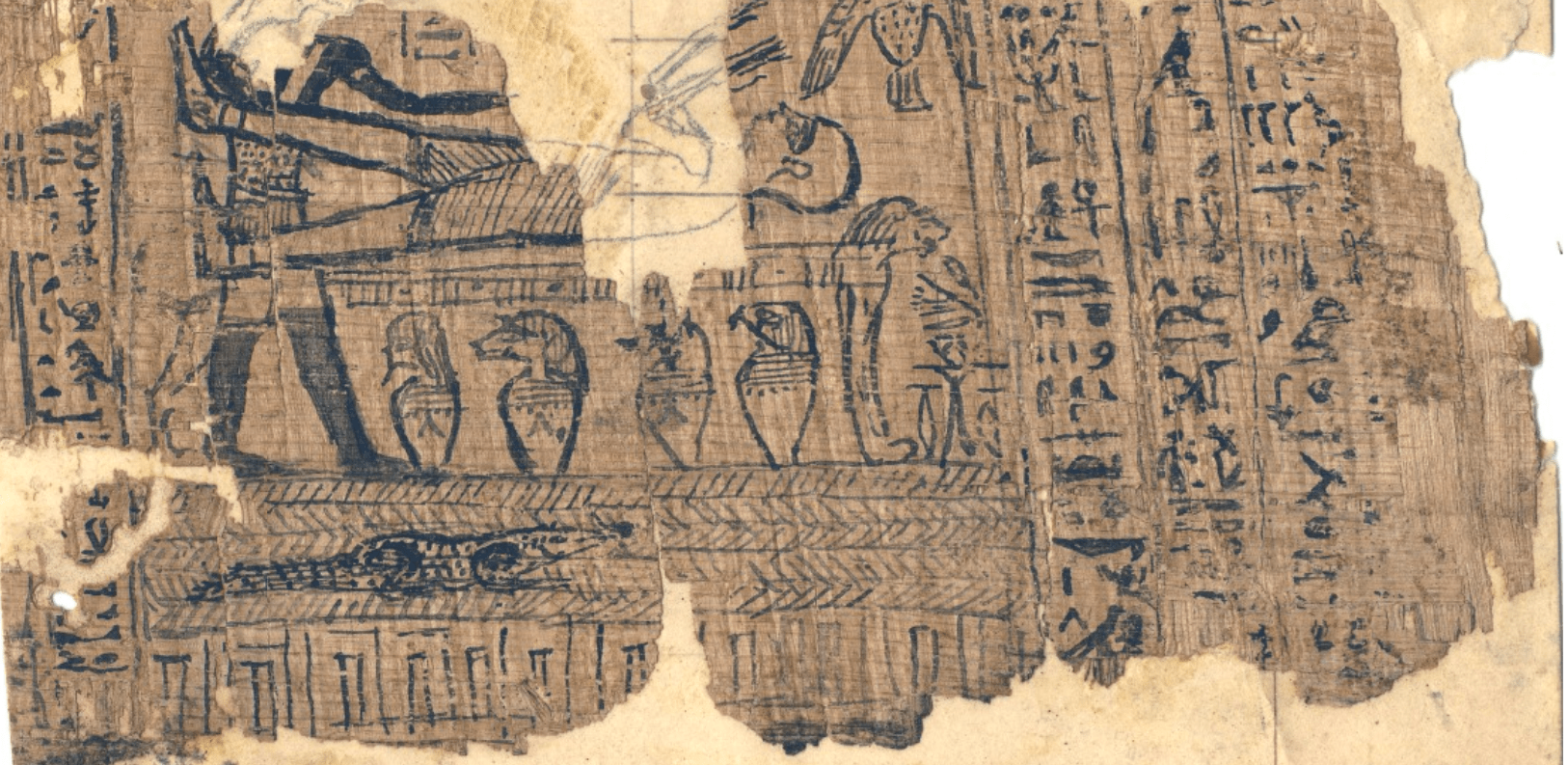

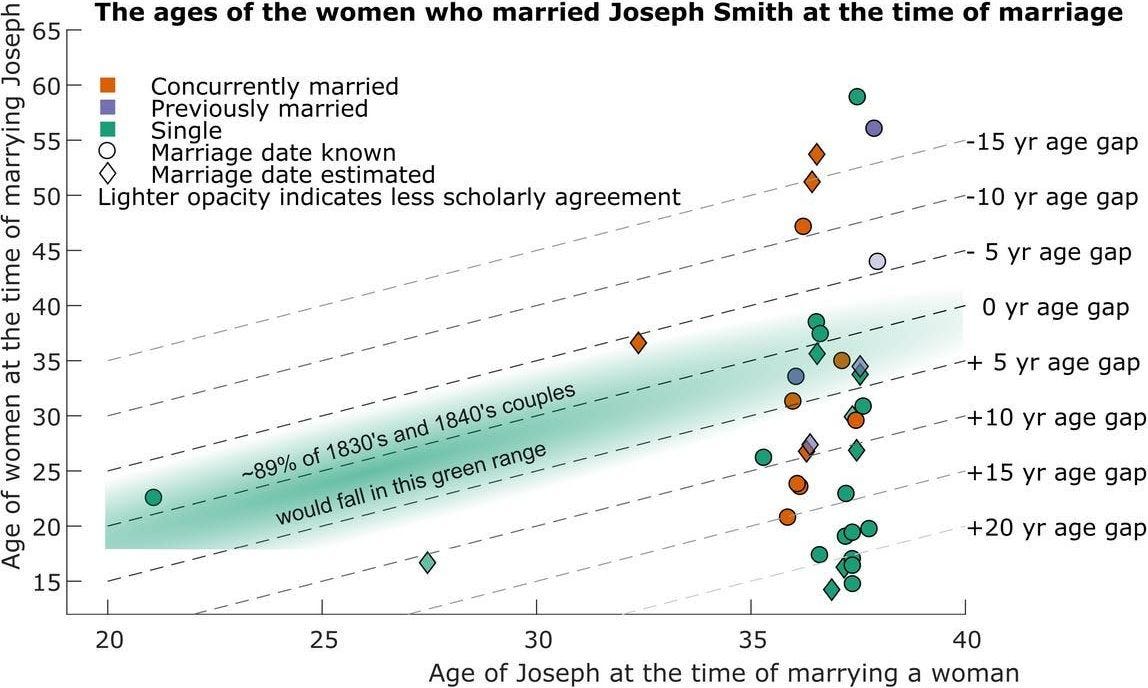

Returning to The Book of Abraham, Joseph Smith published his translation in the church newspaper in 1842, seven years after discovering the papyri. Alongside the text, he included three illustrations copied directly from the original papyrus scrolls, famously known today as the three facsimiles:

These are known respectively as Facsimile Nos. 1, 2, and 3. As you can see, Joseph added small Arabic numerals to each Facsimile, linking parts of them to a commentary he put below where he explained what each part depicts. More on that later.

Two years after publishing the Book of Abraham, Joseph was killed by an angry mob after trying to run for president of the United States and engaging in various other ambitious exploits (there are so so many). Following Joseph’s death, the mummies and papyri remained with one of his widows, which he secretly had like 30-40 of. Nobody is totally sure on the exact number, but you know you have many wives when they constitute an entire dataset you can make plots from:

Joseph’s widow sold the papyri scrolls in 1856 to a museum in Chicago, after which they were all lost to the Great Chicago fire of 1871. Which sucks a lot because if we still had them Egyptologists could translate them to see if they correspond with Joseph’s translation. Can you imagine what would happen if we had the original papyri? Either Mormonism would be dead or it would be a major world religion, but instead they disappeared just like the golden plates the Book of Mormon originated from.

At least we still have the facsimiles Joseph copied over from the papyrus scrolls. Couldn’t these be checked to see if Joseph’s description of them corresponds with expert consensus? This is what Episcopal bishop Franklin Spalding from Utah was thinking at least. So in 1912 he sent copies of the three facsimiles to eight of the world’s most prominent Egyptologists and Semitic scholars. Their responses were not that flattering. Renowned Egyptologist James H. Breasted stated:

“Joseph Smith’s interpretation of them as part of a unique revelation through Abraham, therefore, very clearly demonstrates that he was totally unacquainted with the significance of these documents and absolutely ignorant of the simplest facts of Egyptian writing and civilization.”

Another one stated:

“I return herewith, under separate cover, the ‘Pearl of Great Price.’ The ‘Book of Abraham,’ it is hardly necessary to say, is a pure fabrication. Cuts 1 and 3 are inaccurate copies of well known scenes on funeral papyri, and cut 2 is a copy of one of the magical discs which in the late Egyptian period were placed under the heads of mummies. There were about forty of these latter known in museums and they are all very similar in character. Joseph Smith’s interpretation of these cuts is a farrago of nonsense from beginning to end. Egyptian characters can now be read almost as easily as Greek, and five minutes’ study in an Egyptian gallery of any museum should be enough to convince any educated man of the clumsiness of the imposture.”

In November 1912, Spalding published their responses in a widely circulated pamphlet called “Joseph Smith, Jr., As a Translator” and it caused massive controversy. Critics felt they finally had the smoking gun to prove Joseph was a fraud, while Mormon defenders argued that the scholars might be biased or that Egyptian could be interpreted in multiple ways, or Joseph’s hired printer didn’t faithfully represent the originals, or Joseph took some freedom to alter the original to better convey God’s message, and probably many other explanations.

Spalding’s pamphlet is impressively empathetic and carefully crafted. To me it reads like a banger substack post except in slightly dated prose. The opening dedication goes:

“To my many Mormon friends — who

are as honest searchers after the truth

as he hopes he is himself — this book

is dedicated by the author.”

Then he begins the pamphlet with “If the Book of Mormon is true, it is, next to the Bible, the most important book in the world.” and then continues for a few pages talking about the importance of the Book of Mormon… if it were true. Then he empathizes with the unfair treatment of Mormon apologists in the public discourse:

“A rather careful reading of the controversy leads this writer to the conclusion that the Latter-day Saints (Mormons) set an example of dignity and courtesy which their opponents rarely followed. And yet, in the adoption of this unfair method, critics of Mormonism were but following the example of other defenders of their faith against novelty in religion”

My experience speaking with Mormons has been in a similar vein. On average, they’re kinder, more hard working, more moral and more educated, than the average non-Moromon. In my many hours of discussion with a dozen different Mormon missionaries, I’ve received only thoughtful responses and kindness, even when presenting them with quite challenging arguments. It has been hard for me to not feel inspired by the light in their eyes, which I rarely see otherwise in my largely atheistic circles. I know they’re trying to up-sell me, but still, true religious zeal is hard to fake.

Spalding moves on to make this separate point in the opening of Chapter 3:

“The eighth article of faith of the Church of Jesus Christ of Latter-day Saints distinguishes between the correctness of the translation of the Bible and of the Book of Mormon. While the Bible is accepted as the Word of God, “so far as it is correctly translated,” there is no such caution with reference to the Book of Mormon, but the statement, “We also believe the Book of Mormon to be the Word of God,” is without qualification”

This is the stance Muslims take towards the Quran. Standard Islamic teaching tells us that the Quran is the literal uninterpreted word of God transmitted word for word in Arabic to the Prophet Muhammad through the angel Gabriel, and then perfectly preserved over time by Muslims memorizing the entire book until they eventually wrote it down. According to mainstream Islam, the Arabic Quran is entirely free from mistakes or contradictions because any mistake would mean God made a mistake, which is impossible. Eternal, flawless, and fully preserved:

“This is the Book about which there is no doubt, a guidance for those conscious of God.”

— Qur’an 2:2

Now this is a heavy burden to carry! Only a single mistake and the entire prophecy crumbles into dust. Rationalists know that the more falsifiable claims you make, the more points you stand to gain or lose. If Bible-thumpers can use “human error” to excuse the more problematic parts of the Bible, then they earn fewer points for the more convenient ones. If a Muslim says “everything in the Quran is word-by-word from God” then perfection is demanded, but if it is perfect, it should be strong evidence in favor of Islam.

The Book of Mormon is more like the Quran than the Bible in this sense: God gave the translation to Joseph directly, word for word. Which means the text better be God damn flawless. Or at the very least free of flaws so damning even thousands of apologists cannot come up with a plausible sounding explanation for why it’s not actually a flaw.

By the way, I’ve not yet told you how Joseph interpreted the facsimiles, nor how expert opinion differs. But it’s not that bad, otherwise Mormonism wouldn’t be flourishing long after all these discoveries. I’ll let you be the judge though.

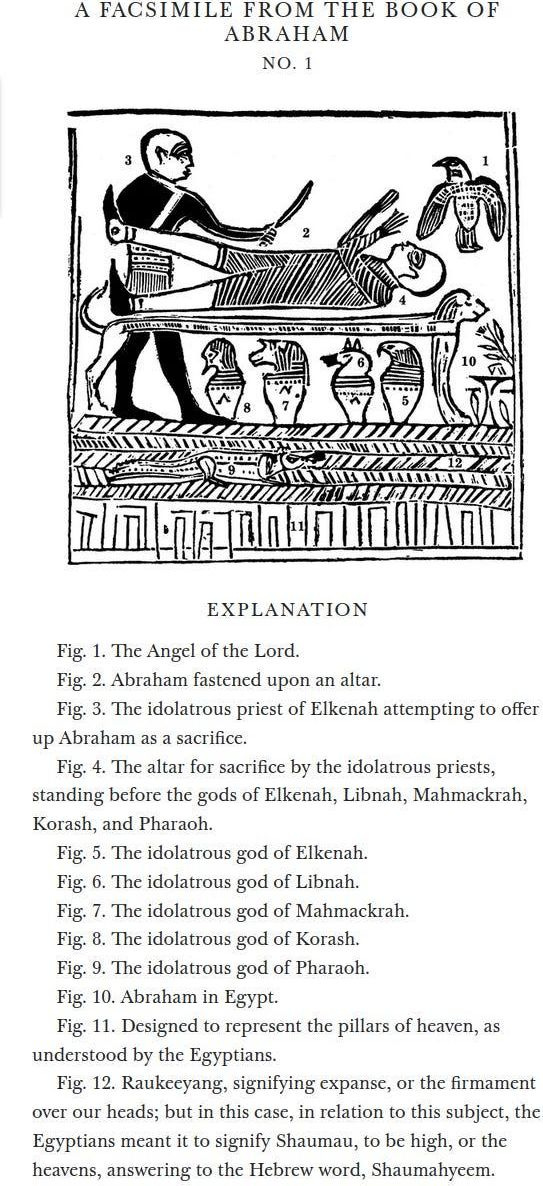

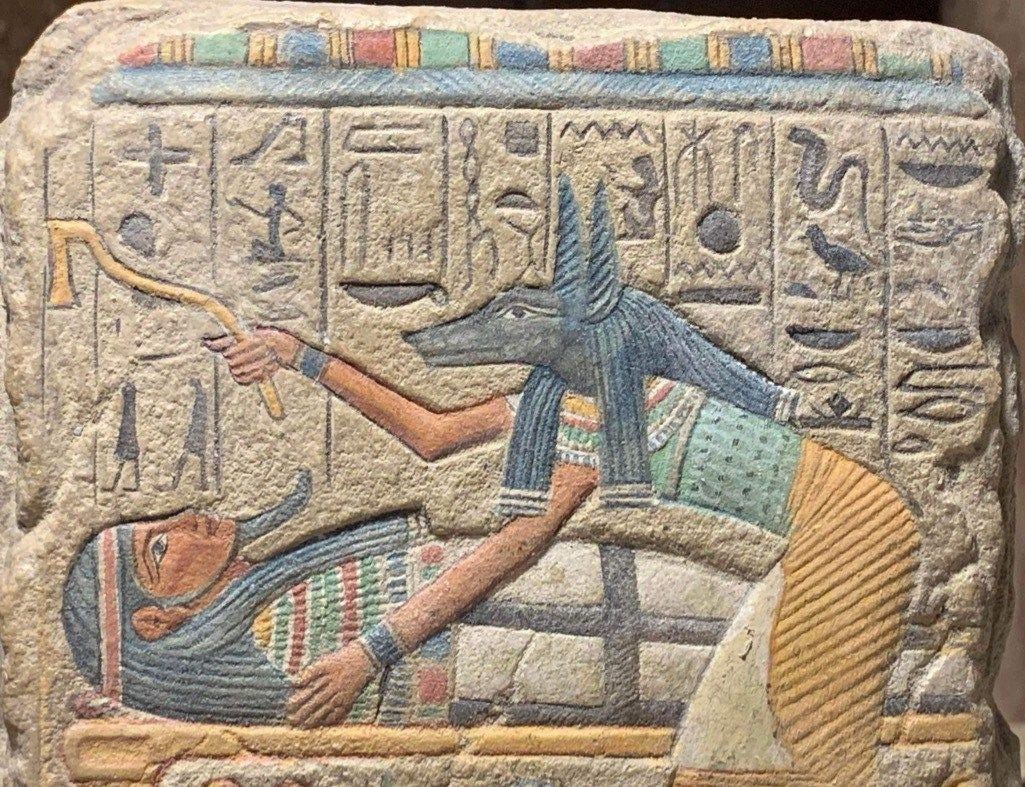

Here’s Facsimile No. 1 again, also known the “lion couch scene”:

Below it you see Joseph’s interpretation of the various parts. The scene is also referenced in the beginning of the main text:

“And it came to pass that the priests laid violence upon me, that they might slay me also, as they did those virgins upon this altar; and that you may have a knowledge of this altar, I will refer you to the representation at the commencement of this record.”

Abraham 1:12

This is in the voice of Abraham, where he goes on to explain how he got bound to an altar in some pagan Egyptian temple, about to be ritually murdered by the priest of Elkenah, while the Angel of the Lord descends from above to rescue him.

Why did contemporary Egyptologists disagree? Primarily because this type of scene is quite typical in Egyptological studies:

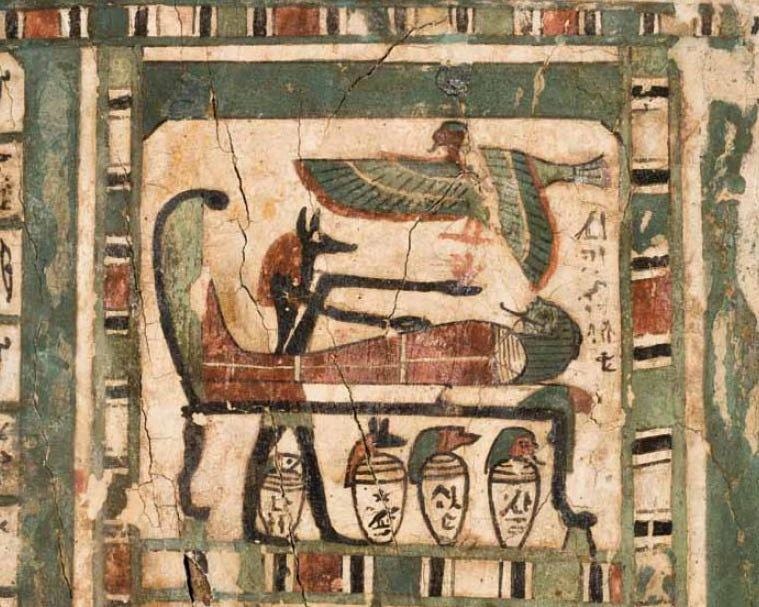

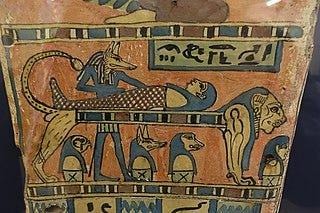

The standard interpretation of this scene is that the Egyptian god Anubis is embalming a deceased man on a funerary bier to prepare him for the afterlife. Beneath the bier you’ll spot the canopic jar set Sally didn’t get for her sweet sixteen, which hold the organs removed during embalming.

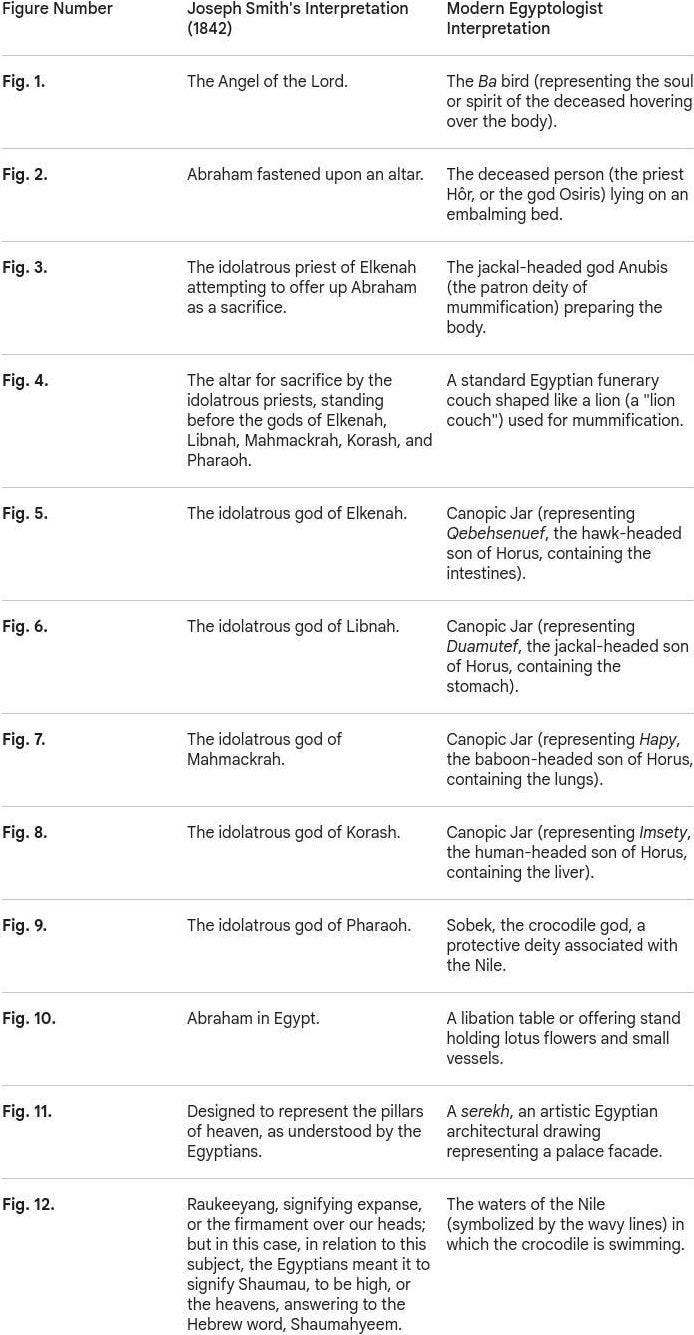

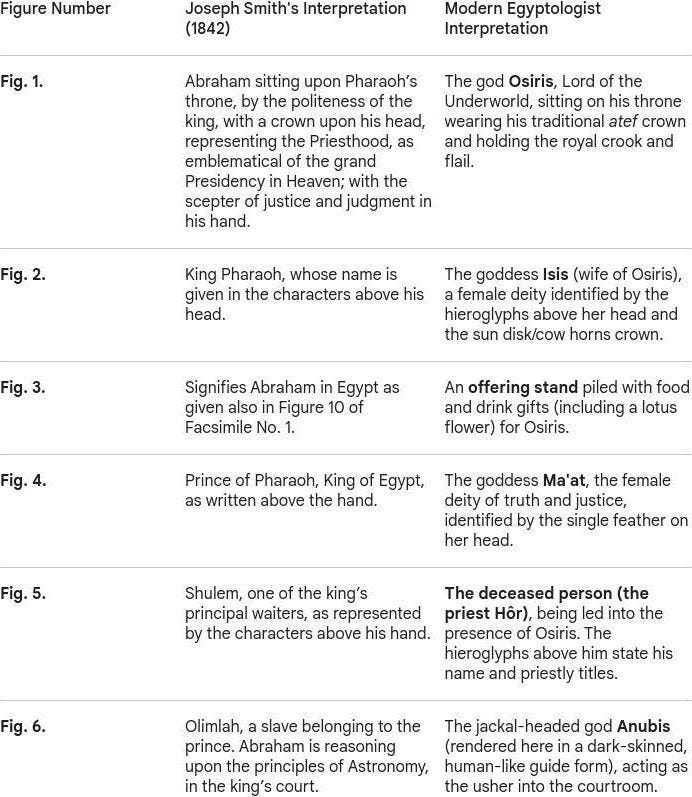

Here is a full table comparing Joseph’s interpretation with the Egyptological one:

It’s understandable that Egyptologists would be frustrated by Joseph’s claims, but aren’t they a touch overconfident? First, the figure with the knife has no jackal head, so it’s clearly not Anubis. Second, he’s holding a knife, not a jar or strange axe like the figures in the reference images above. Third, the flying bird-creature in Facsimile 1 looks quite different from the bird-creature in the reference. And fourth, it’s Egypt. Is it really so outrageous that someone might have performed a sacrifice on an embalming table?

The canopic jars are an oddity, granted: they look fairly standard, yet Joseph identifies them as non-standard Egyptian gods. But how did he know they were gods in the first place? And there’s another wrinkle, who actually drew the facsimiles? We know Abraham “wrote… upon papyrus” with his own hand, but not that he drew the illustrations himself. If he hired some Egyptian artist off the street, the artist might well have leaned a bit too much on his usual repertoire, producing something that looks more like a generic funerary scene than what was actually intended.

Couldn’t Egyptologists also be doing shallow pattern-matching? Mapping something they’ve seen many times onto something that merely resembles it, and gaining undue confidence from the match? Doctors routinely misdiagnose for exactly this reason. A rare disease whose symptoms somewhat overlap with a common one gets mistaken for the common one. Why couldn’t Egyptologists fall into the same trap?

This is getting too tiring, let’s move on.

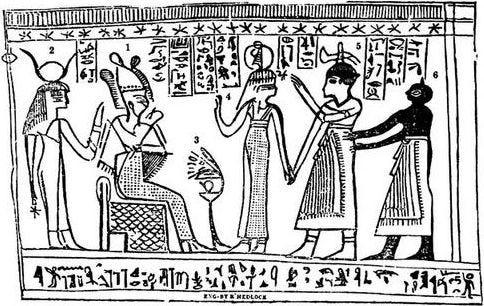

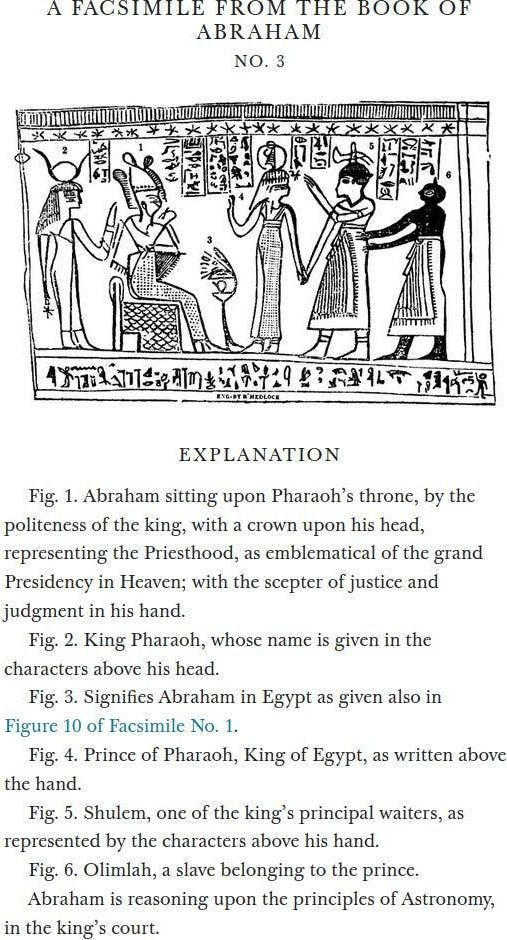

Now to Joseph’s interpretation of Facsimile No. 3:

Why did Egyptologists disagree? One reason is that this type of scene is quite typical in Egyptological studies:

Apparently this is a common Egyptian funerary vignette. Egyptologists identify it as a presentation scene from the famous Book of the Dead. The text written on it serves as a permit granting the deceased (in the case of Facsimile 3 an Egyptian priest named Hôr) the right to breathe, speak, and exist among the gods in the afterlife.

How do they know it’s for a priest named Hôr? If you look closely at Facsimile 3. you can notice that it has Egyptian text written on it:

This text can be translated into English! The Egyptians captioned every single thing Joseph captioned and they can be directly compared.

Here is a full table comparing Joseph’s interpretation with the Egyptological one:

What can we notice about this table? Going figure by figure:

Abraham is the God of the underworld.

King Pharaoh is the wife of Abraham God of the underworld.

(generic description of the scene)

Prince of Pharaoh, King of Egypt is the goddess of truth and justice.

One of the king’s principal waiters is the deceased priest Hôr.

A slave belonging to the prince (who is also the goddess of truth and justice) is the jackal-headed god Anubis.

At first glance, this one seems a bit harder to square. The last column of Egyptian text literally translates to “Recitation by Anubis, who makes protection, foremost of the divine booth…” while Joseph says it’s a slave belonging to the prince.

But it’s not really that hard to square. Again, Abraham isn’t claimed to have made the facsimiles himself, only to have written the main text. So if he (or someone later) commissioned an Egyptian artist to render it for him, then the artist, being Egyptian, did what Egyptian artists do: rendered the scene using the conventions of his time. The artist added some standard Book of The Dead captions, but Joseph knew what was really being depicted since God told him. This makes sense, the dark-skinned person that Egyptologists claim is Anubis doesn’t even have a Jackal head:

The same expert pattern-matching problem from before: of course it looks like a standard scene. Egyptian art always looks like a standard scene. That doesn’t tell you what specific event it commemorates.

We’ll not get anywhere with circumstantial evidence. Maybe we can look at facsimile No. 2.

Interlude 2.

Around 1819, a teenage Joseph Smith walked three miles from his family’s farm to meet a girl named Sally Chase. Sally was, at the time, the most famous seer in Palmyra, New York.

Treasure-digging was a real industry in rural upstate New York. The Spanish, supposedly, had buried gold and silver caches across the region during forgotten colonial expeditions, and any farm boy with a shovel and the right spiritual gift might be the one to find them. The right spiritual gift usually involved a “seer stone” (also called a “peep stone”) a small smooth rock that, when consulted correctly, would reveal the location of the treasure to the seer’s spiritual eye. Hundreds, possibly thousands of Americans worked in the trade.

Methods varied. Some practitioners used divining rods. Some interpreted thrice-spoken dreams. Some conjured elemental spirits. The Palmyra method, which Sally Chase had popularized in her own neighborhood, went like this: you’d put a stone into your hat, put your face into the hat to block out the light, and in the resulting darkness the stone would glow, revealing the treasure.

Sally Chase had a small green stone mounted in a little wooden paddle. She used it to find lost cattle, missing pocketbooks, stolen tools, etc. Locals paid her for the consultations. According to one neighbor, “Sallie Chase, a Methodist, had a peep stone and people would go for her to find lost and hidden or stolen things.” According to a school-friend, “she would place the stone in a hat and hold it to her face.” Joseph’s own mother, Lucy Mack Smith, wrote in 1845 that Sally had “found a green glass, through which she could see many very wonderful things.”

The Mormon historian D. Michael Quinn put it most bluntly: “Until the Book of Mormon thrust young Smith into prominence, Palmyra’s most notable seer was Sally Chase.”

The teenage Joseph visited Sally, looked into her green stone in her hat, and was excited to discover that he could see visions too. He told her there was another stone, his own stone, buried under a tree about a hundred and fifty miles away. A few years later he acquired stones of his own and went into business.

Between 1822 and 1827, Joseph conducted at least 18 documented treasure digs across upstate New York and northern Pennsylvania. Paying clients would hire him, Joseph would do the hat thing, and the clients would dig where he told them to. The Smith family had a small home industry going: Joseph Smith Sr. owned a ceremonial dagger inscribed with astrological and occult symbols, which the family used to draw protective circles around dig sites to ward off the guardian spirits that, according to local treasure-digging lore, were known to protect buried hoards.

A persistent feature of these expeditions was that no treasure was ever actually recovered. Shovels would strike something solid, but then an “enchantment” would kick in, the treasure would slip deeper into the earth, and the guardian spirit would win that round. This was a standard explanation across treasure-digging culture and the diggers found it broadly satisfying.

In late 1825, a well-off farmer named Josiah Stowell hired Joseph (having, in his words, “heard that he possessed certain keys, by which he could discern things invisible to the natural eye”) to help locate a lost Spanish silver mine in Pennsylvania. The dig went the way they all went: shovels striking, treasure slipping. Stowell remained a believer. Stowell’s nephew, Peter Bridgeman, did not.

In March 1826, Bridgeman had Joseph arrested. New York state law specifically outlawed “pretending… to discover where lost goods may be found,” and Joseph was hauled before Justice Albert Neely in Bainbridge, NY, on a charge of being “a disorderly person and an imposter.”

The court record listed the defendant by profession: “The Glass Looker.”

For the next 145 years, mainstream Mormon historians insisted that no such trial had ever happened. The Mormon historian Francis Kirkham wrote in 1942:

“A careful study of all facts regarding this alleged confession of Joseph Smith in a court of law that he had used a seer stone to find hidden treasure for purposes of fraud, must come to the conclusion that no such record was ever made, and therefore, is not in existence… If any evidence had been in existence that Joseph Smith had used a seer stone for fraud and deception, and especially had he made this confession in a court of law as early as 1826, or four years before the Book of Mormon was printed, and this confession was in a court record, it would have been impossible for him to have organized the restored Church.”

Mormon scholar Hugh Nibley, the Church’s most respected apologist, wrote in 1961 that if such a court record were ever to surface, it would be “the most damning evidence in existence against Joseph Smith”, “the most devastating blow to Smith ever delivered.” Nibley was confident the record didn’t exist.

In 1971, a Presbyterian minister named Wesley Walters walked into the basement of the sheriff’s office in Norwich, NY, and pulled out the original 1826 court bills from Justice Neely’s docket. They were authentic. The trial had happened. Joseph had testified, admitting under oath that he had used a seer stone to look for buried treasure, though he claimed he had since given the practice up. It hurt his eyes, he said.

The Church now acknowledges the trial on its official website. The current framing is that “Joseph Smith, like others in his day, used a seer stone to look for lost objects and buried treasure,” and that “as Joseph grew to understand his prophetic calling, he learned that he could use this stone for the higher purpose of translating scripture.”

From 1822 to 1826 the stone-in-a-hat method found buried Spanish silver. From 1827 onwards it found the word of God. Joseph never put down the technique, but he did upgrade the clientele.

Which his old seer-teacher Sally Chase took notice of. In September 1827, just after Joseph claimed to have recovered the golden Book of Mormon plates from a buried stone box on a nearby hill, Sally Chase put her green stone into her hat one more time. She told her brother Willard and a group of friends that the plates were hidden in the Smith family’s workshop. The men broke in, ripped up the floorboards, but found nothing but a decoy box. The plates? They were hidden in the loft.

Joseph had been doing the hat thing for eight years by then.

He was the better seer.

Part 3.

Back to Facsimile No. 2.

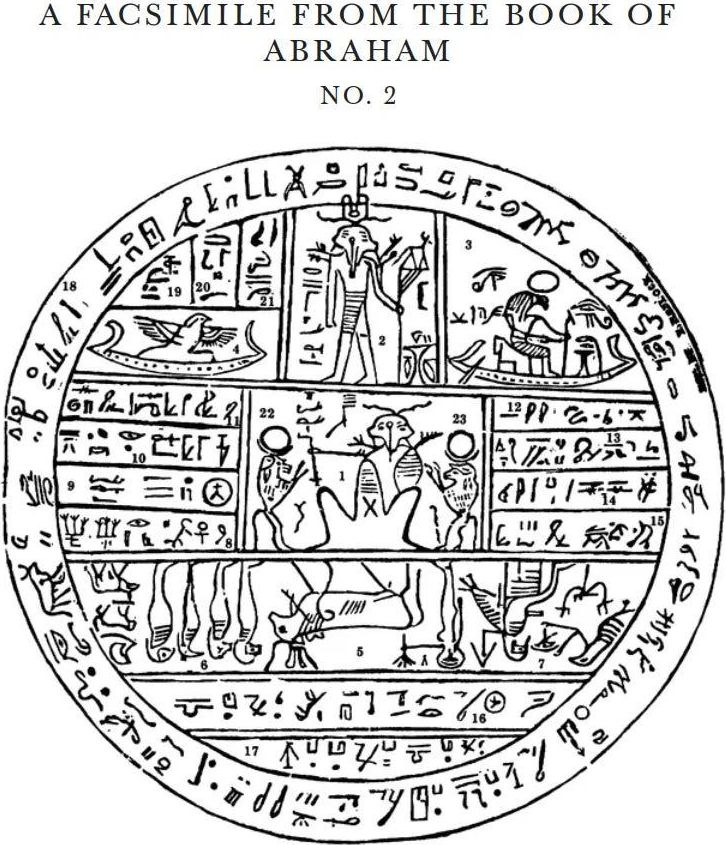

This one is round:

No need to read Joseph’s captions for now, but I’ll place them here for reference:

So why did Egyptologists disagree? Again, this kind of object is standard:

This time it’s so standard I had difficulties telling at first glance whether they are actually different or just varying quality copies of the same thing.

This type of disk is called a hypocephalus. The name is Greek for “under the head.” Hypocephali were small magical discs, usually papyrus or linen, occasionally bronze, that were placed under the head of a mummy. They functioned as a kind of divine pillow whose purpose was to keep the head of the deceased warm and illuminated in the afterlife, wrapped in a magical aura of fire. There are roughly 158 surviving hypocephali in museums around the world. They are all variations on the same basic theme. As you can tell Joseph’s seems like a normal example of one.

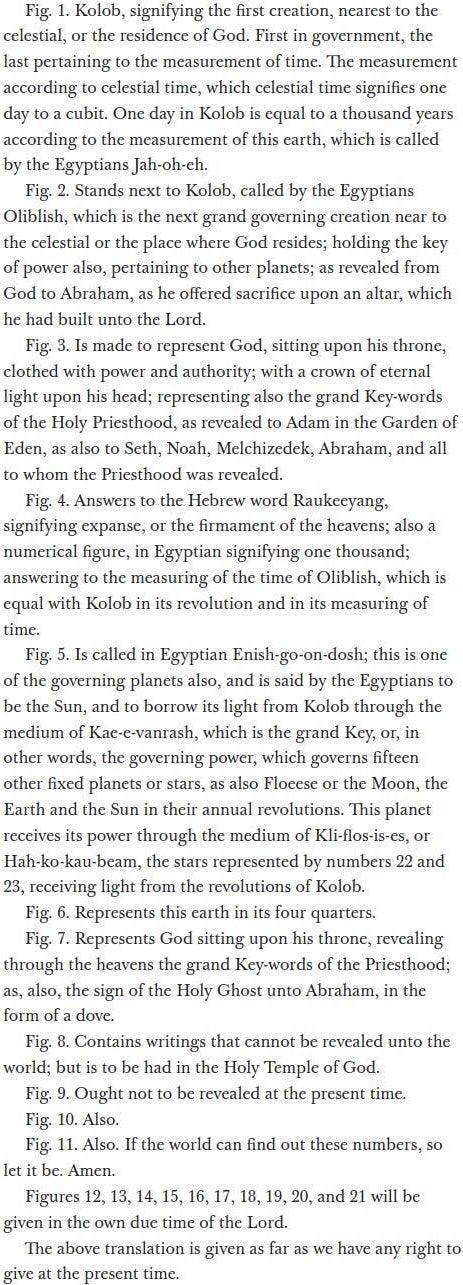

Joseph’s interpretation is that the disc is a star map describing the celestial hierarchy of the universe. Twenty-one figures are labeled, like the facsimiles before it, with confident captions. The central seated figure (Fig. 1) is “Kolob, signifying the first creation, nearest to the celestial, or the residence of God.” Other figures are identified as governing planets, the sun, the moon, lesser celestial bodies. A few explanations are flagged as too sacred to share publicly “to be had in the Holy Temple of God”. Some other explanations “will be given in the own due time of the Lord.”

There’s a bit much to unpack here, so I’ll just highlight the most notable parts. Otherwise you can read this table if you’re interested:

Firstly, as with Facsimile no. 3. This one contains a lot of Egyptian text, but Joseph doesn’t give us the translation to any of it, he just explains the figures 1 through 7. Egyptologists have no issue translating it though, except for this part:

This part is a bit problematic to translate because the characters seem to make no sense in the context of facsimile 2. The Egyptologists in Spalding’s pamphlet pointed this out, but nobody knew how they got there. A mystery!

And, yes. The text that is understandable contradicts the interpretations Joseph did give. But, we already have an explanation for that. Egyptian artists being Egyptian artists. Just Google hypocephali, they all look identical! For example this figure appears in most of them:

Here’s the corresponding figure (Fig. 7) from Facsimile 2:

According to Joseph this is God. Not an Egyptian one, but the God of the bible, sitting upon his throne. According to all Egyptologists (including Mormon ones) this is Min, Egyptian god of fertility, sitting with a fully erect penis.

It might seem a bit outrageous by Christian standards to depict God with a fully erect penis. The Mormon Church at least thought so, which is why they removed the penis in all their post-1902 printings of the Book of Abraham. This wasn’t widely advertised, many members never realized anything had been altered. They did put it back in 1981, and today it’s still there on the official version on the Church’s website.

How do we square this?

Let’s assume Abraham commissioned some Egyptian artist to make Facsimile 2. And then the artist made a completely normal looking hypocephalus seemingly for some random dead guy, because Egyptian artists had no ability to make anything else, not even the ability to exclude an erect penis. If we assume this, then everything makes sense. What is Abraham supposed to do? He’s got to work with what he has. If God can just tell Joseph how to interpret the illustration, then it doesn’t matter what’s actually shown or written on it, as long as, in the reader’s eyes, it somewhat resembles the scene in the story.

Still though… God with an erect penis? Maybe we can try this comment I found on a forum:

“It’s NOT a phallus! There are no sitting hieroglyphics with an erect phallus (that I’ve ever seen). Also, it’s coming out of his belly! There are many hieroglyphics like that showing an arm or both arms coming out of the person’s belly. Look at the many hieroglyphics with an erect phallus and you’ll see they get it right-it originates at the groin, not the belly. Also (as if all that wasn’t enough) if you’ve been through the temple, you’ll recognize the positions of the arms). It’s not a phallus, it’s his right arm!”

I’ve got to admit, he’s right. The 4 other examples I posted all seem to have a more groin-originating phallus.

Again, only mixed evidence. Let’s move on.

Interlude 3.

In April of 1843 a year after the Book of Abraham was published, a man named Robert Wiley was digging in an ancient burial mound near the town of Kinderhook, Illinois, when he came across six small brass plates bound together with an iron ring. The plates were bell-shaped, covered in mysterious characters resembling none of the known ancient scripts, and obviously really old:

Word spread quickly. Within days the plates were on their way to Nauvoo, Illinois, where Joseph Smith was now headquartered, because if anyone could read mysterious ancient writing it was the guy who had already done it twice.

Joseph was excited. His scribe William Clayton wrote in his journal:

“President J. has translated a portion and says they contain the history of the person with whom they were found and he was a descendant of Ham through the loins of Pharaoh, king of Egypt, and that he received his kingdom from the Ruler of heaven and earth.”

A descendant of Ham through Pharaoh. Inscribed on brass. Buried in an Illinois mound. Translated by the prophet on sight. Mormon publications celebrated the find, here was independent archaeological vindication of Joseph’s translation gift. The Times and Seasons, the church’s newspaper, ran an enthusiastic article. Plans were made to publish a full translation.

Then Joseph got busy with other things (presidential campaign, polygamy, the ongoing question of whether the people of Illinois were going to riot and burn his city down, the various ongoing things) and the translation was shelved. A year later he was dead. The Kinderhook plates faded from active discussion in the church, but they remained part of the Mormon historical record as a translation Joseph had begun.

Can you guess what happened next?

In 1879, a man named Wilbur Fugate wrote a letter explaining that he, Robert Wiley, and a third local man named Bridge Whitton had forged the plates as a hoax. They had cut the plates from sheet brass, etched the “ancient” characters with acid, aged them with rust, and buried them in the mound specifically to see if Joseph would fall for it. Fugate’s letter was published. Mormon authorities dismissed it as the bitter fabrication of an apostate.

Then the story was lost to time.

Until in 1980, the one surviving Kinderhook plate (the other five had been lost over the intervening century) was subjected to metallurgical analysis at Northwestern University. The plate was 19th-century brass. The characters had been etched with nitric acid. The composition was inconsistent with anything ancient and entirely consistent with Fugate’s 1879 confession.

The plates were a forgery. The forgers had said they were a forgery. The forgery had been confirmed by an independent laboratory. And Joseph had translated them confidently, on sight, as containing the history of a descendant of Pharaoh.

Is this a problem for Mormonism? At first glance it might really seem like that, but if you look a bit into it, not really. I’ll tell you why.

Part 4.

When the Mormons bought Chandler’s Abraham papyri in July 1835, Joseph did not put them in a drawer. He had work to do.

Over the following months, he and his scribes produced a remarkable body of documents trying to systematize what they were doing with the papyri. These are collectively known today as the Kirtland Egyptian Papers, and they are the closest thing we’ll ever have to a fly-on-the-wall view of Joseph’s translation process. They have been preserved, digitized, and published in full as part of the Joseph Smith Papers Project. You can read them online for free in Joseph’s handwriting and the handwriting of his scribes, which is a more direct line on a prophet’s working methods than most religions can offer.

The crown jewel of the collection is a document called the “Grammar and Alphabet of the Egyptian Language.”

That’s the title written across the title page in W.W. Phelps’ careful handwriting. Phelps was Joseph’s primary scribe in this period, and the two of them were apparently quite serious about the project. The GAEL, as it’s normally abbreviated, is a kind of Egyptian-English dictionary. On the left side of each page is an Egyptian character. On the right side is the meaning of that character, in English. This is what a typical page would look like:

There are several hundred entries. It is exactly the kind of document a serious translator of ancient Egyptian would produce, methodically built up character by character, the way Champollion was doing it in France around the same time.

Imagine the implications. If the GAEL is valid, every museum on Earth needs to call Salt Lake City. Champollion can pack up his Rosetta Stone and go home. Joseph has the master key.

There’s something peculiar about it though.

The GAEL has, for each character, up to five degrees of meaning. The first degree might be a short gloss like “the first man, or Adam.” The second degree expands it. The third degree expands it more. By the fifth degree, the same single squiggle is being unpacked into something like “Adam, the first man, the father of all the human family, having dominion over the whole earth in the patriarchal order, blessed of God in the day in which he was created.” One Egyptian character, dozens to hundreds of English words:

But maybe ancient Egyptian was special. Maybe ancient Egyptian had a kind of secret high-density mode, accessible only to prophets, where a single character could contain a paragraph at the first degree and a longer paragraph at the fifth.

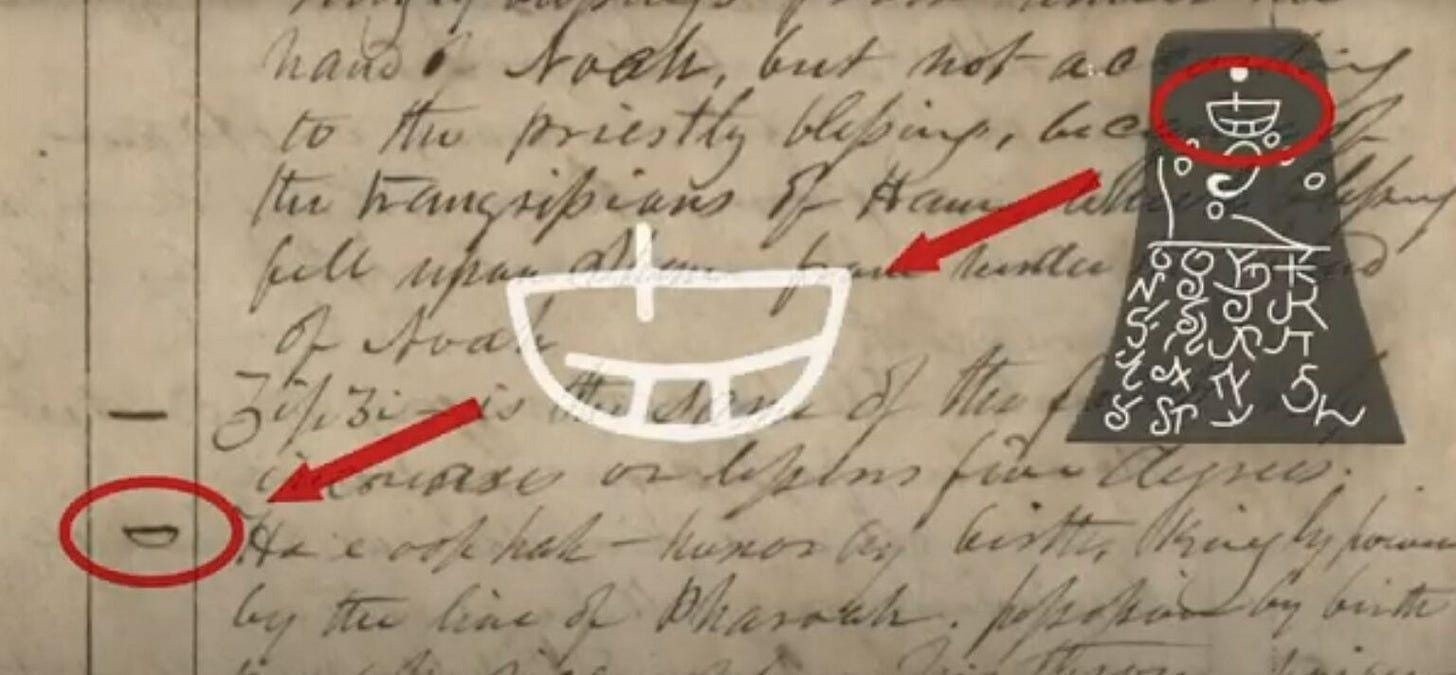

The GAEL is actually what perfectly explains the Kinderhook plates scandal. In 1980, Mormon historian Stanley Kimball noticed something striking. One of the characters on the Kinderhook plates closely resembles a character in the GAEL:

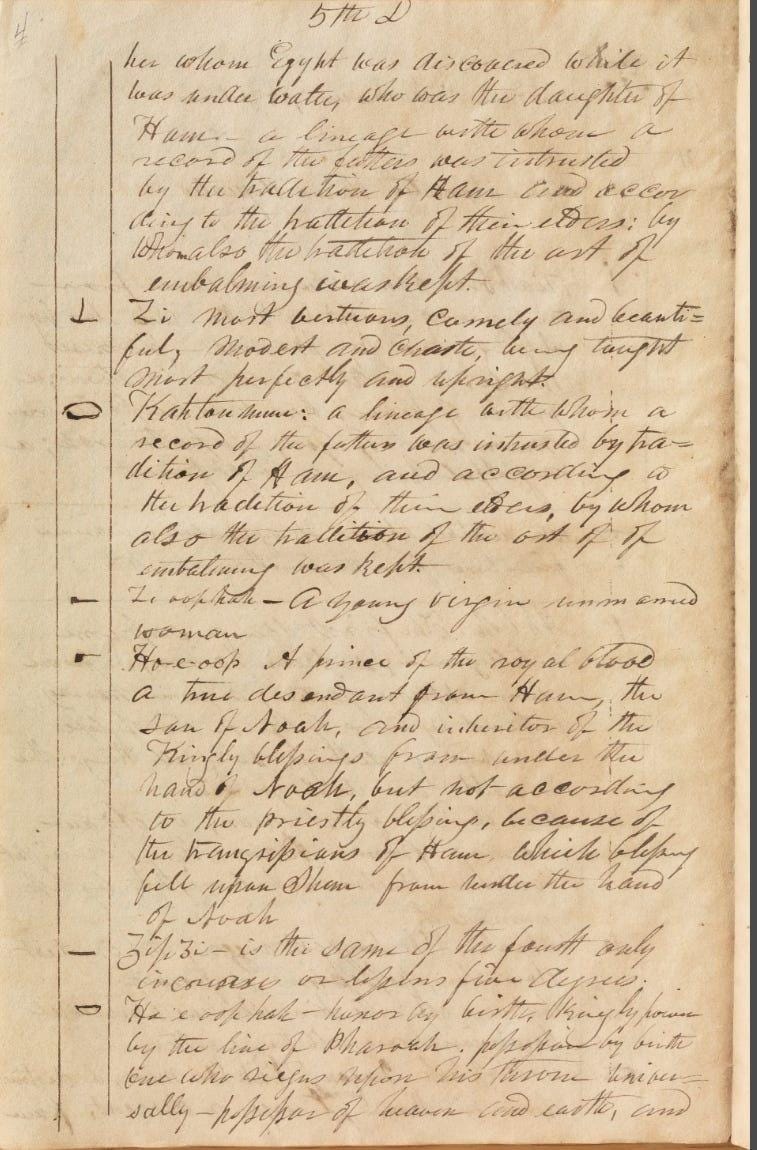

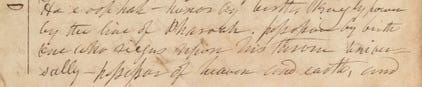

The GAEL entry for that character is defined as:

“Ho e oop hah — honor by birth, kingly power by the line of Pharoah. possession by birth one who riegns upon his throne universally — possessor of heaven and earth, and of the blessings of the earth.”

Compare that to what Joseph’s scribe Clayton recorded Joseph saying:

“a descendant of Ham through the loins of Pharaoh, king of Egypt, and that he received his kingdom from the Ruler of heaven and earth.”

The “descendant of Ham” bit comes from Clayton’s journal, not from the GAEL. The apologetic argument bridges the gap by noting that in 19th-century biblical genealogy (Genesis 10), Pharaoh’s line traces back to Ham via Mizraim, so “descendant of Pharaoh” implies “descendant of Ham” to anyone steeped in the King James framework, which Joseph and his scribes were. So the argument is: GAEL gives “kingly power by the line of Pharaoh,” Joseph’s biblically-saturated mind unpacks that as “descendant of Ham through Pharaoh,” Clayton writes it down.

(If this argument is sort of difficult to follow, don’t worry, I agree.)

Joseph didn’t claim revelation. He looked at the plates, recognized a character that resembled one in his reference document, and read off the corresponding entry. This was a secular attempt at translation using a lookup table, the same way you’d use a Latin dictionary. It was scholarly, not prophetic. No witnesses saw him put his face into a hat containing a stone. And the fact that he never produced a full translation supports this. Once he ran out of matchable characters, he had nothing more to say, so the project quietly died.

Nothing to see here, let’s move on.

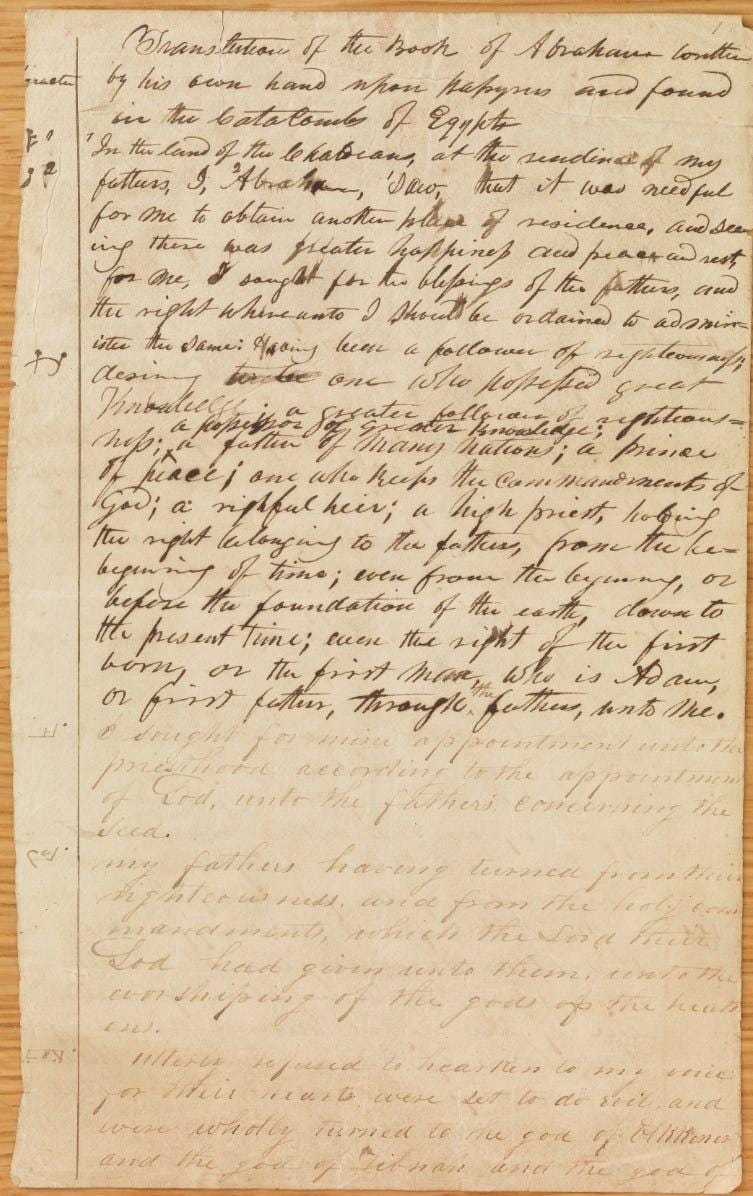

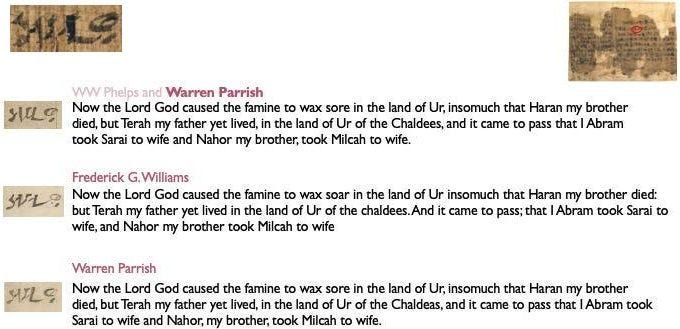

There’s a second set of documents in the Kirtland Egyptian Papers that is more concrete than the GAEL, and harder to make sense of. The Joseph Smith Papers call them “Abraham Manuscript 1,” “Abraham Manuscript 2,” and “Abraham Manuscript 3.” They are working drafts of the Book of Abraham itself, dictated by Joseph and recorded by three different scribes: Frederick G. Williams, Warren Parrish, and W.W. Phelps. They cover the opening chapters of the book that would later be published in the church newspaper in 1842.

The format is identical in all three: there is a left margin and a body. The body contains the English text of the Book of Abraham. The left margin contains Egyptian characters lined up with the English passages they correspond to. Here’s one such manuscript page, the opening to the Book of Abraham:

Damn. We have original documents containing the Book of Abraham manuscript with Egyptian characters in the margin. We can just translate the characters and check if Joseph was correct.

Clearly a single Egyptian squiggle doesn’t translate to “And it came to pass that the priests laid violence upon me, that they might slay me also, as they did those virgins upon this altar; and that you may have a knowledge of this altar, I will refer you to the representation at the commencement of this record”

So how do we square this? Apologists have easy answers to this:

The Book of Abraham was not translated, but inspired. The explanation goes: Joseph would look at an Egyptian character, then he would receive a paragraph of English text from God. The Egyptian character is unrelated to the English paragraph, except as a sort of catalyst. The Egyptian was, in a sense, irrelevant to the revelation. It was a holy relic that triggered the vision, but not the source the way a French novel is the source of its English translation.

The Kirtland Egyptian Papers, on this view, are a separate project. They were Joseph and his scribes’ attempt to reverse-engineer the Egyptian language. They already had the English from God. They had the papyri from Chandler. They were curious about how the two were connected, so they sat down and tried to work it out. The GAEL is the in-progress notebook of that side project. The Abraham manuscripts are scribal study aids, in which the scribes paired English passages they already had with characters they were trying to memorize. They are not, despite appearances, translation drafts at all.

Makes sense right? Joseph looks at an Egyptian character, God reveals an English paragraph to him, so naturally Joseph thinks the English paragraph is supposed to be the translation of the Egyptian character. Joseph didn’t claim to have a scholarly understanding of Egyptian, but a prophetic one. Therefore, all he can do is try to scholarly reverse-engineer the language from his prophetic visions.

You might think it’s a bit weird that God would confuse Joseph like this. Joseph did claim translation of ancient Egyptian, going so far as to construct a grammar for it. Wouldn’t it be easier to just beam prophecy into his mind or speak to him through a burning bush or something? Maybe God thought “translation of ancient Egyptian” would sell better in Joseph’s time, although thinking about marketing in that way doesn’t seem like a very godly thing to do.

Also, how do we square this with:

“A Translation of some ancient Records that have fallen into our hands from the catacombs of Egypt. The writings of Abraham while he was in Egypt, called the Book of Abraham, written by his own hand, upon papyrus.”

Whatever Joseph received in English should correspond with something Abraham literally wrote down upon papyrus by his own hand. What exactly did Abraham write down on papyrus? The characters we saw in the margins? But they don’t correspond to the English text according to Egyptologists. Maybe Abraham just wrote down a completely ordinary funerary document in Egyptian because he knew God would, regardless of the literal meaning of the characters, give Joseph whatever message he wanted.

Another apologetic response is that Joseph and the scribes were just goofing around, adding random characters to the margins for some unrelated reason, and making the GAEL as a fun hobby project. Then the real Egyptian that Abraham wrote down in his own hand upon papyrus is not the characters in the margins of the Abraham manuscripts, but some other characters that were on the real Abraham papyri lost in the 1871 Chicago fire.

Nothing more to see here. Let’s move on.

Interlude 4.

In 1836, the Mormons were running into a familiar problem. The Church had grown to several thousand members, mostly recent converts who had been gathering to Kirtland, Ohio, on the Prophet’s instructions. They were building a temple, which is expensive. They had bought a great deal of land, also expensive. They had a fast-growing population that needed jobs, housing, and food, all expensive. Joseph himself was personally on the hook for tens of thousands of dollars, much of it from land speculation that hadn’t yet paid off, plus a $25,000 loan for a single shipment of merchandise.

What does any reasonable religious founder/prophet do in this situation?

Start a bank of course.

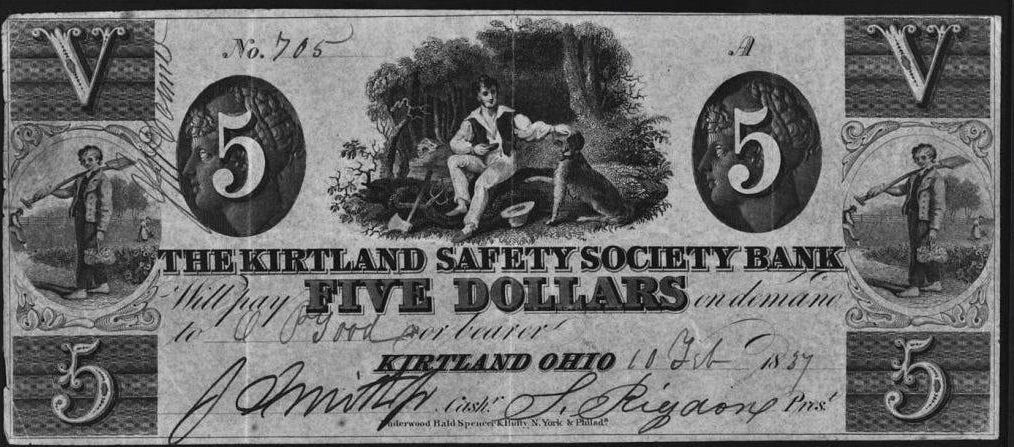

In November 1836, Joseph and a handful of church leaders drew up articles of incorporation for the Kirtland Safety Society Bank. They commissioned beautiful banknotes engraved with eagles, classical figures, and the signatures of Joseph Smith as cashier and Sidney Rigdon as president.

They ordered a safe. They hired tellers and ordered ledgers. The inner circle of the Smith family also took the opportunity to subscribe to large amounts of stock, most of it bought on credit, which is the part that should probably make you nervous as a depositor.

Then they sent Orson Hyde to the Ohio state legislature to get the bank chartered. The legislature said no. It is unclear exactly why. Possibly there was significant anti-Mormon sentiment in the statehouse, possibly the legislature was just denying lots of bank charters that year as part of a broader Jacksonian skepticism toward banks. Either way, no charter. Without a charter, the bank could not legally operate as a bank in Ohio.

Joseph’s solution was GENIUS.

He had the bank’s printed banknotes overstamped with the prefix “ANTI-” so that they now read “KIRTLAND SAFETY SOCIETY ANTI-BANKING COMPANY,” and called the institution an anti-bank, with himself serving as anti-cashier and Rigdon as anti-president. Then they opened for business on January 2, 1837, and began issuing the notes as currency.

It wasn’t a bank, legally, so the Ohio legislature has nothing to do with it. But the notes are still backed by specie (coined money made of precious metal) and real estate, so they’re as good as bank notes. Now the anti-bank can ask people “please, accept our notes as money” and people did, at least at first, partly because Joseph announced by revelation that the anti-bank would “swallow up all other banks” and grow to become the most powerful financial institution on the continent. If this is starting to sound like a 2022 whitepaper, keep reading.

There was a small inventory issue with the specie. According to several witnesses, including the scribe Warren Parrish (the same Warren Parrish whose handwriting appears all over the Book of Abraham manuscripts), the vault contained large wooden boxes labeled with figures like “$1,000,” stacked impressively along the walls. Joseph would lead visiting investors through the vault, gesture at the boxes, and demonstrate that the institution was solidly capitalized. The boxes were filled with sand, lead, old iron, and stone, with a thin layer of silver coins on top of each one to maintain plausible deniability in case someone insisted on a closer look.

Things went well for about three weeks. The notes circulated, locals accepted them, the anti-bank looked legitimate. Then a coalition of competing local businessmen, most of whom disliked the Mormons for unrelated reasons, started systematically buying up the notes at a discount and presenting them back to the anti-bank in bundles, demanding redemption in specie. The anti-bank ran out of specie almost immediately. The notes started trading at a discount on the open market. By February they were at about fifty cents on the dollar. By summer they were essentially worthless. Local merchants who had been paid in them ate the loss.

In May 1837, the broader Panic of 1837 hit the United States and made everything much worse. Banks failed across the country, specie payments were suspended nationwide, and the credit economy of the frontier seized up. But the Kirtland Safety Anti-Banking Company had already failed by then, of its own structural issues, before the Panic could provide cover. Joseph resigned as anti-cashier in June. The institution wound down across the summer and was effectively dead by autumn. Joseph and Rigdon were each later fined $1,000 by an Ohio court for illegal banking. They did not pay.

Worst of all was the fact that a lot of Joseph’s followers had invested in the anti-bank not because they thought it was an attractive business proposition but because the Prophet had said by revelation that it would succeed. When it didn’t, this raised an awkward theological question. Joseph addressed it directly. From the pulpit, he explained that the revelation about the bank’s success had been conditional on the saints being righteous, and apparently the saints had not been righteous enough, which was why God had withdrawn his support, which was why the bank had failed. The failure was not Joseph’s fault. It was the bank-holders’ fault for being insufficiently holy.

This argument did not land equally well with everyone. Many of the bank-holders had lost their life savings. They began leaving the Church in significant numbers, and notably, the people leaving were not the marginal recent converts: they were senior leaders. A third of the Quorum of the Twelve Apostles defected over the next several months, several of them publicly accusing Joseph of being a fallen prophet, at least one of them confronting Joseph in the Kirtland temple itself in an episode that involved drawn bowie knives. Oliver Cowdery, the man who had served as primary scribe for the Book of Mormon translation, who had been there for the foundational visions, who was technically the second-highest figure in the early Church, was excommunicated in 1838 over a combination of the bank failure and his uneasiness about Joseph’s emerging polygamy. He spent the next decade outside the Church before returning, quietly, near the end of his life.

In January 1838, with creditors closing in and warrants out for him over the banking violations, Joseph fled Kirtland in the middle of the night on horseback together with Rigdon. They rode hard for Missouri, where the main body of the Mormons had been independently gathering, and re-established Church headquarters. Most of the remaining Kirtland Mormons abandoned the temple they had spent years and most of their savings building, and followed him west within months.

How do we square this?

It has already been squared. God told Joseph the bank would succeed conditional on the investors being good and godly. Joseph conveyed this to the investors without the “being good and godly” condition because that’s understood. Obviously God wouldn’t bless unholy men. Consequently the anti-bank went anti-bankrupt.

Part 5.

Let’s take stock. At this point in the story we have, on the table:

An ancient Egyptian text written by Abraham on papyrus, translated by a prophet

The original Abraham papyri destroyed in a fire in 1871

Three facsimiles, copied before the fire, that every Egyptologist who has looked at them since calls a standard funerary scene.

Three draft manuscripts of the translation with Egyptian characters in the left margin at a ratio that no real human language has with English

A “grammar” of the Egyptian language Joseph said he was writing, which bears no resemblance to actual Egyptian grammar

A prior career of treasure-digging via seer stones in hats

A subsequent incident, post-Abraham, of confidently translating known forged plates.

Victorian-Crypto Pump-and-Dump Anti-Banking scheme.

All of these have explanations. The grammar? A side project. The margin characters? Scribal exercises. The Egyptologists? Possibly biased, possibly pattern-matching. Abraham’s hired artist? Sloppy. Kinderhook? Joseph hastily uses a private lookup table, not actual revelation. The anti-bank? Conditional revelation, saints insufficiently righteous.

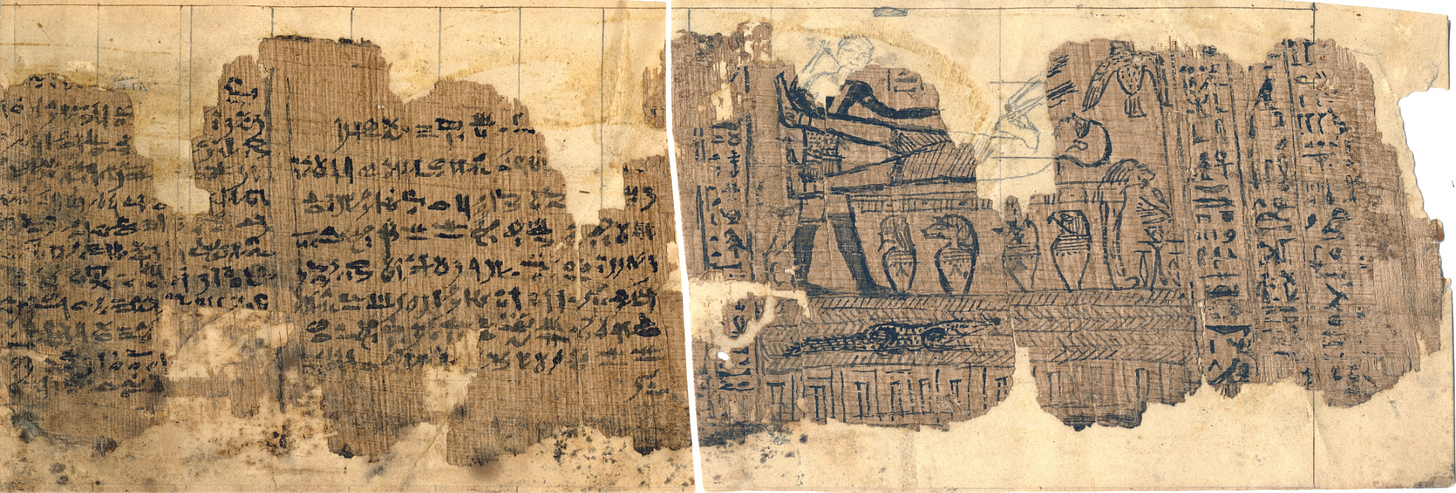

What we actually need to settle this is the source. The actual papyrus. Then either Joseph’s English matches what’s on it, or it doesn’t, and the matter is done. Unfortunately the papyri burned in the Great Chicago Fire of 1871…

This might’ve been a predictable plot twist, but yes, someone found it:

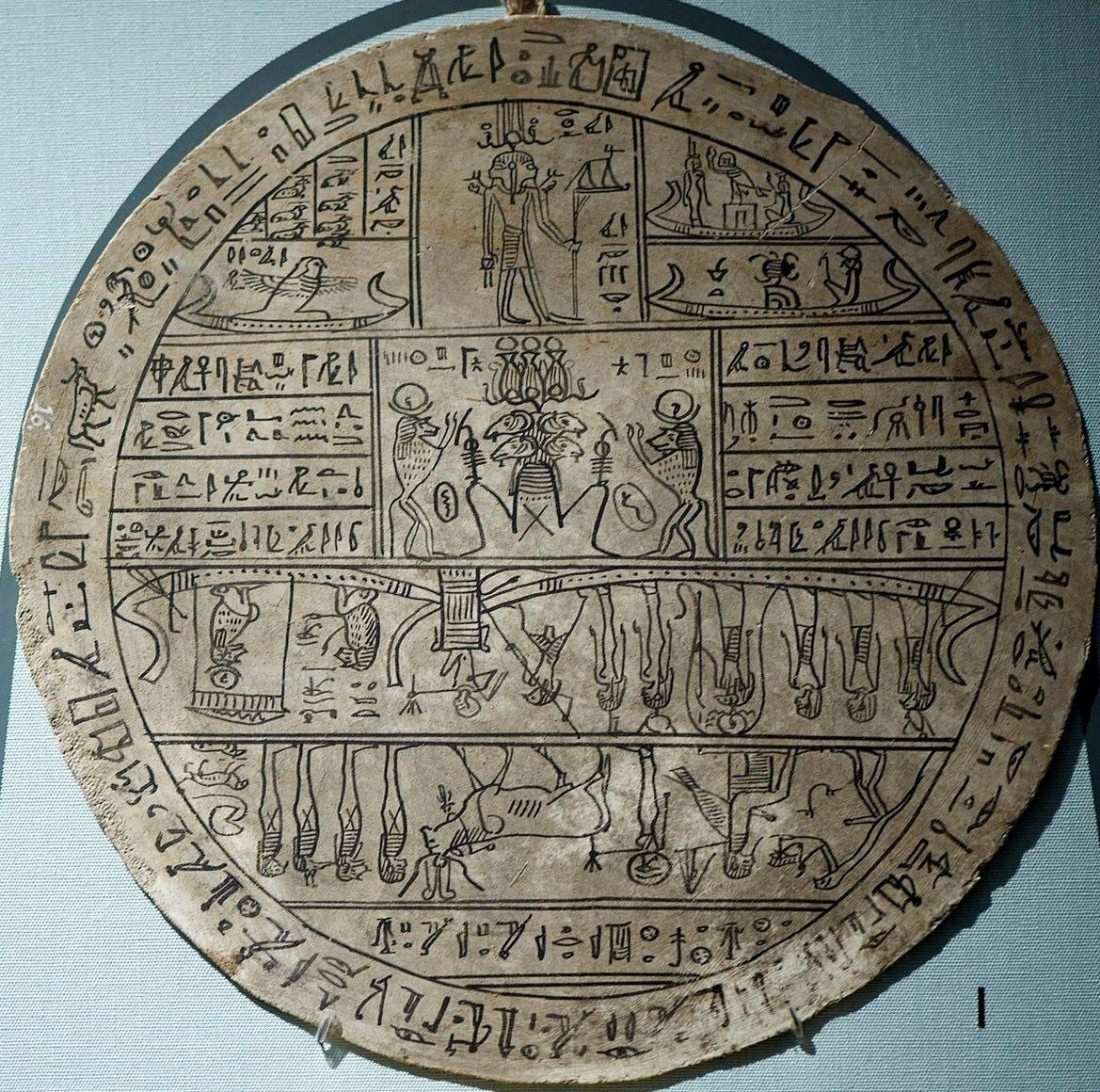

In May 1966, Dr. Aziz S. Atiya, a professor of Middle Eastern history at the University of Utah, was doing research at the Metropolitan Museum of Art in New York. A curator brought him into a back room and showed him eleven fragments of papyrus mounted on stiff backing paper. Atiya looked at them and recognized them instantly. They were the Abraham papyri. They had not burned in Chicago. At some point in the 1850s they had been split off from the rest of the collection, passed through a couple of private owners, and ended up at the Met in 1947, where they had been sitting in a drawer for nineteen years while Mormons everywhere believed they were ashes on the floor of a lakefront museum.

The Met returned the fragments to the Mormon Church on November 27, 1967. The Church published full-page color photographs in its official magazine, the Improvement Era, in early 1968. The reaction inside the Church was, at first, jubilation. The papyri were back. The translation could finally be vindicated.

After 132 years of being theoretically falsifiable but practically untestable, the Book of Abraham was suddenly checkable. You could just look.

The translation took about five minutes, in the sense that any competent Egyptologist could read it on sight. Klaus Baer at the University of Chicago and Richard Parker at Brown University published translations within months. Mormon Egyptologist Hugh Nibley, the Church’s most respected apologist, the same Hugh Nibley who told us in 1961 that the 1826 court record didn’t exist, also studied the fragments and produced a translation. The translations agree. Mormon, non-Mormon, believer, skeptic. Egyptian is a known language. These were standard documents. There is no controversy about what they say.

They are fragments of a text called the Book of Breathings, also known as the Document of Breathing Made by Isis. The Book of Breathings is a shortened, late-period derivative of the much older Book of the Dead. It is a funerary text, placed with a mummy, intended to help the deceased breathe, speak, eat, and move freely through the underworld. Hundreds of Books of Breathings survive in museum collections worldwide. They are mostly identical to each other, with the deceased’s name swapped in. The one Joseph bought from Chandler was made for an Egyptian priest named Hôr. It dates to roughly 150 B.C.

The dating of the papyri is a small inconvenience. Abraham, by traditional biblical dating, lived around 2000 B.C. So for these papyri to have been written by Abraham in his own hand, Abraham would have had to wait fifteen hundred years after his death to pick up a reed pen. This is harder to wave away than the items above. Even by the most generous estimates of biblical chronology, you can’t close a 1,500-year gap with a sloppy artist.

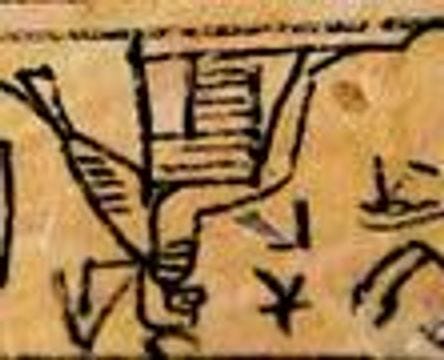

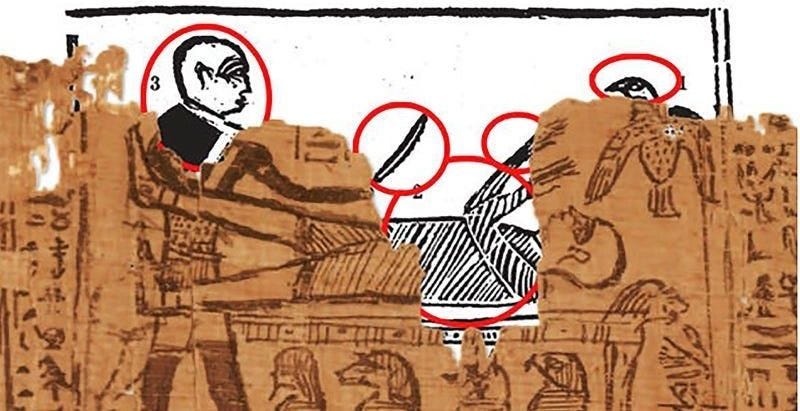

As you can see in the papyri, we also got the original source for Facsimile 1. The lion couch scene. The published Facsimile 1 woodcut matches the surviving fragment line for line, except there were some missing parts. The original papyrus is damaged. There are sections torn away. In the published 1842 facsimile, the missing parts have been filled in by Reuben Hedlock, the engraver Joseph hired to produce the woodcut, working under Joseph’s direct supervision. We can now compare, side by side, what the papyrus actually showed and what Joseph chose to put in the gaps:

The standing figure with the knife, which Joseph identified as “the idolatrous priest of Elkenah attempting to offer up Abraham as a sacrifice,” is missing its head. Joseph drew it as a bald human male. In every other surviving lion-couch scene from Egyptian funerary art, that figure is Anubis, and Anubis has a jackal head. The hovering bird-creature, which Joseph identified as “the angel of the Lord,” is also damaged. Joseph drew it with a full bird head, beak and all. In every parallel scene, that figure is the ba, the soul of the deceased, drawn as a bird with a human head. The altar beneath has gaps. Joseph drew Abraham bound on it. In every parallel scene the figure on the couch is the deceased being embalmed, not bound and conscious.

So we at least have the original papyrus that Facsimile 1 came from. Do we have the source of the Book of Abraham text?

Remember Abraham 1:12:

“And it came to pass that the priests laid violence upon me, that they might slay me also, as they did those virgins upon this altar; and that you may have a knowledge of this altar, I will refer you to the representation at the commencement of this record.”

The commencement of this record. The facsimile is at the beginning of the Book of Abraham. By Joseph’s own framing, the Egyptian text on the papyrus immediately adjacent to Facsimile 1 should be the start of the Book of Abraham itself.

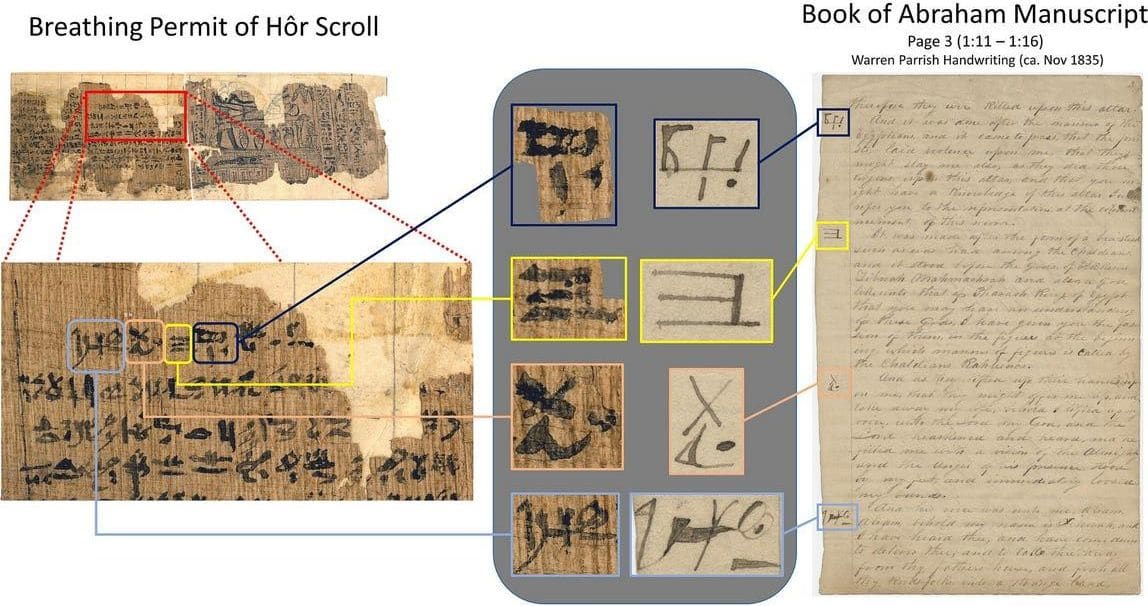

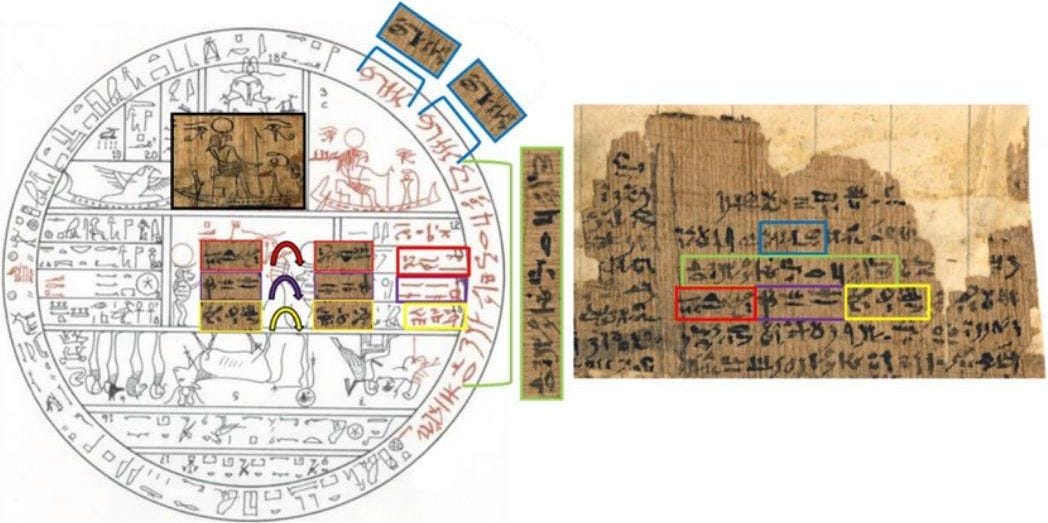

Egyptologists then went looking at the Abraham Manuscripts. The working drafts in the Kirtland Egyptian Papers we covered earlier. Those had Egyptian characters in the left margin and English passages in the body. Where had the margin characters come from?

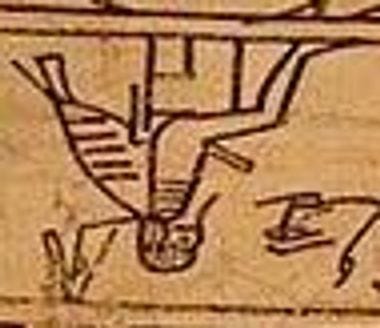

It turned out you could just take the surviving papyrus, the same fragment that sat next to Facsimile 1 on the original scroll, read right-to-left like Hebrew, and find every margin character from the Abraham Manuscripts, in order, on the page:

Joseph’s scribes had been copying them off in sequence and lining them up with whatever English Joseph was dictating at the time.

There is no longer a way to plausibly say “well, the artist did what artists do,” because we are not looking at an artist anymore. This papyrus fragment was written by Abraham in his own hand. If Abraham wrote down the characters on the papyrus with his own hand, why did he write down a completely standard funerary document in Egyptian script?

The Church has answers to all of this. It has had nearly sixty years to figure out a position, and the position has converged on two theories.

The first is the missing scroll theory. The papyri we recovered are real, but they are not the source of the Book of Abraham. Eyewitnesses in the 1830s described “a long roll” of papyrus. The surviving fragments are short. Therefore: the actual Book of Abraham was on a portion of the scroll that has since been lost, and what we have are unrelated funerary documents that happened to be stored alongside it. The character match between the papyrus and the Abraham Manuscripts is, on this view, some kind of scribal indexing artifact, or coincidence, or post-hoc gesture. The Egyptian characters being right next to Facsimile 1? Could also be a coincidence.

This was somehow a comfortable position until Mormon scholars themselves started calculating. Andrew Cook and Christopher Smith published a paper in 2010 calculating, from the diameter of the surviving scroll and the way papyrus rolls wind, how much length could plausibly be missing. Their answer was about 56 centimeters. Not enough to hold the Book of Abraham. The math has been contested by other Mormon scholars, notably John Gee at BYU, who argues the scroll could have been much longer. The dispute has the flavor of motivated reasoning racing against motivated reasoning, and the casual reader, after about twenty pages of cross-referenced scroll diameter equations, finds themselves once again drifting toward the soft consolation of “we don’t have all the answers.”

The second theory is the catalyst theory. The papyri are not the source at all. They were just the trigger. Joseph received the Book of Abraham by direct revelation from God, the same way he received the Book of Mormon, by putting his face in a hat. The papyri were a holy object that catalyzed the revelation, but the revelation itself had no specific textual connection to them. The match between margin characters and the papyrus is then irrelevant. Joseph was producing revelation, the scribes were copying down characters as keepsakes or memorization aids, and the entire “translation” framing was a quaint 19th-century misunderstanding by everyone in the room, including, at times, Joseph himself.

This is now more or less the official Church position. The Church’s Gospel Topics essay on the Book of Abraham, published quietly in 2014, leans heavily on it. The essay concedes that the surviving fragments do not contain the Book of Abraham, that the dating problem is real, and that the relationship between the fragments and the published text is, in the essay’s own careful phrasing, largely a matter of conjecture.

The catalyst theory is great, but it has the smaller disadvantage of being almost completely unrelated to what Joseph said he was doing. Joseph wrote the title page himself:

“A Translation of some ancient Records that have fallen into our hands from the catacombs of Egypt. The writings of Abraham while he was in Egypt, called the Book of Abraham, written by his own hand, upon papyrus.”

There is no catalyst here. There is a translation. Of Abraham’s writings. By Abraham. On papyrus. The papyri are not a trigger for a revelation, they are the source, and they were written by Abraham personally. Joseph spent eight years working on the Kirtland Egyptian Papers, building a grammar, lining up English to Egyptian, character by character. He did not behave like a man receiving free-floating visions. He behaved like a man who thought he was translating an ancient text.

Now we’re in the position where one of the following must be true:

Joseph was simply mistaken about what he was doing. He looked at the papyrus, which is a standard funerary document, and then God revealed to him translations from another papyrus scroll that Abraham had actually written with his own hand, containing its own set of 3 facsimiles that simultaneously line up with both standard funerary scenes and Abraham’s story at the same time. Meaning, God wildly misled Joseph, in a highly convoluted way, into making him say and do things that are not only highly embarrassing (interpreting God himself with an erect penis), but which makes it seem like he was making it all up.

Or, he was making it all up.

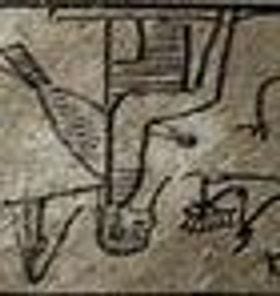

I think theory 1 Is plausible. Although it has some issues. Remember those weird out-of-place characters from Facsimile 2.?:

Egyptologists at the time couldn’t really make sense of them in that context. The reason is that they had just been copy pasted from the papyrus fragment:

Not only copy pasted, but like, turned upside down, or pasted twice in a row for no specific reason.

How did Joseph caption these characters that he had himself put there? This:

Which is ironic because he published his supposed translation of them in the main Book of Abraham text. Here is one of these characters from the papyrus and the corresponding margin character from 3 different drafts of the Abraham manuscript from 3 different scribes:

This is the same character he pasted into Facsimile 2 twice in a row:

So he takes characters from the papyrus, pastes it into the facsimile, then says the translation will be given in the due time of the Lord, and then publishes a translation of the same characters in the main Book of Abraham text together with the facsimile itself.

Anyone can check this for themselves. All the original documents are on display in high quality scans by the Church.

If he mistakenly thought he was receiving a translation of the characters because God presented English to him while looking at Egyptian, then why do this weird copy pasting of characters you’ve already received a translation to and then saying the translation will be given in the due time of the Lord?

How do we square all of this?

It’s still easy. Otherwise, Mormonism wouldn’t be going strong:

Interlude 5.

By 1843, Joseph was no longer the awkward farm boy with a peep stone in a hat. He had been leveling up for fifteen years. Nauvoo, Illinois, where the Mormons had relocated after being expelled from Missouri at gunpoint in 1839, was now one of the largest cities in the state, with a population rivaling Chicago. Joseph was its mayor, its chief magistrate, the editor of its newspaper, the proprietor of its general store, the trustee-in-trust of the Church, and the lieutenant general of its private militia. The militia was called the Nauvoo Legion. It had something like 2,500 men under arms. The entire United States Army at the time numbered around 8,500.

He had also, by this point, been sealing himself to additional wives at a pace that would make the chart back in Part 2 unreadable if I had included the timestamps. The polygamy was officially secret. Joseph publicly denied it, repeatedly, from the pulpit:

“What a thing it is for a man to be accused of committing adultery, and having seven wives, when I can only find one.”

Privately he had about thirty, including the wives of several of his loyal apostles, who were dispatched on missions and informed of the sealings upon their return.

Most of this was extremely illegal. Polygamy was a felony. The Nauvoo Charter, which Joseph had wrested from the Illinois legislature, gave the city’s municipal court the power to issue writs of habeas corpus and free Mormons from any non-Mormon arrest warrant, a power normally reserved to federal judges. Joseph was, increasingly, running a small theocratic principality inside the state of Illinois, and the state of Illinois was starting to notice.

In January 1844, Joseph announced his candidacy for President of the United States. His platform proposed abolishing slavery (funded by the sale of public lands), annexing Texas and Oregon, abolishing imprisonment for debt, and reestablishing a national bank with branches in every state. He dispatched around 600 missionaries to campaign for him across the country, which was, by some margin, the largest organized presidential field operation in American history to that point.

Two months later, in March 1844, Joseph also founded the Council of Fifty. This was a secret body whose stated purpose was to function as the constitutional government of the Kingdom of God that would shortly be established on Earth. On April 11, by unanimous motion of the Council, Joseph was formally received “as our Prophet, Priest & King.” The minutes of these meetings were considered so sensitive that the Church did not allow scholars to read them until 2016. They are now published in full as part of the Joseph Smith Papers Project, alongside the Kirtland Egyptian Papers.

To summarize: in the spring of 1844, Joseph Smith was simultaneously the mayor of a semi-independent Mormon city-state, the lieutenant general of a private army roughly a third the size of the United States Army, a declared candidate for President of the United States, the prophet of a fast-growing international religion, the husband of approximately thirty women, the chief judge of a municipal court that could nullify any state arrest warrant against him, and the secretly-anointed earthly king-priest-prophet of the millennial Kingdom of God.

This is the part of the story where you should expect things to begin going wrong, and they did.

Inside the church, a faction of senior leaders had figured out the polygamy. William Law, who was Second Counselor in the First Presidency (the third-ranking office in the entire Church, after Joseph and Sidney Rigdon), discovered that Joseph had proposed plural marriage to William’s wife Jane while William was away on a Church mission. Several other senior Mormons had made similar discoveries. They confronted Joseph privately. They got nowhere. So in June 1844, they pooled their money, bought a press, and founded a newspaper called the Nauvoo Expositor, with the express purpose of publishing the truth about Joseph Smith.

The first and only issue of the Nauvoo Expositor appeared on June 7, 1844. It documented the polygamy. It documented the Council of Fifty. It accused Joseph of using ecclesiastical authority to obtain political power and… bang their wives. The reporting was, in the main, accurate.

Three days later, on June 10, the Nauvoo City Council, with Joseph presiding as mayor, declared the Expositor a public nuisance and ordered it destroyed. That evening, the city marshal led a group of Mormon men to the Expositor office, smashed the printing press with sledgehammers, and burned the surviving copies of the paper in the street.

This was a flagrant violation of freedom of the press, and the rest of Illinois noticed immediately. Non-Mormon newspapers across the state, and then across the country, exploded with coverage. Warrants were issued. Governor Thomas Ford of Illinois ordered Joseph to appear in Carthage, the county seat, to face charges of inciting a riot. Joseph initially declared martial law in Nauvoo, mobilized the Legion, fled across the Mississippi, considered an escape to the Rocky Mountains, then turned around and surrendered. On his way to Carthage he reportedly said: “I am going like a lamb to the slaughter.”

Joseph and his brother Hyrum were held in a second-story room of Carthage Jail beginning June 25, 1844. The “jail” was less a jail than a sturdy stone house with iron bars on one window. The door to the upstairs room could not actually be locked. Once the Smiths were in custody, the charges were upgraded from inciting a riot to treason, preventing bail. Governor Ford personally promised the prisoners they would be safe. Two of Joseph’s followers, who had been permitted visits, smuggled in two pistols.

On the afternoon of June 27, 1844, a mob of approximately two hundred men with blackened faces rushed the jail. They fired through the door. Hyrum was killed instantly, shot through the face. Joseph fired his smuggled pepperbox pistol back through the door, wounding two attackers, then ran to the window. He was shot multiple times, fell out of the second-story window, and died on the ground below. He was thirty-eight years old.

Part 6.

I guess this is the part where we could wrap up with a neat, triumphant moral: Joseph Smith was a fraud, the papyri proved it, and the entire edifice of Mormonism is a monument to human gullibility. But that conclusion is unsatisfying because it fails to explain the graph:

If the success of a religion depended on the epistemic cleanliness of its origin story, the graph should have hit zero in 1912 when Bishop Spalding published his pamphlet. It definitely should have hit zero in 1968 when the papyri fragments were translated. Instead, it kept climbing. Today there are millions of Mormons, disproportionately representing high levels of wealth, education, civic engagement, marital stability, charitable work, charitable giving, self-reported life satisfaction.

This leaves us with a question. Joseph Smith’s translation methodology was, by any standard, a spectacular, multi-car pileup of confirmation bias, post-hoc patching, and literal cut-and-paste forgery. Yet, the culture spawned by this pileup is one of the most highly optimized, high-trust, pro-social engines of human coordination on the planet.

(I can’t help but wonder what would’ve happened if Joseph could muster the strength to not have sex with the wives of all his high-ranking officers. For all we know he might’ve taken over the world.)

How to square this?

A community built on something demonstrably absurd operates on different physics. The default mental posture of every member is rationalization of the common knowledge, and rationalization, once it becomes habitual, runs in the community’s favor. The work of explaining away the next embarrassment has already been done a hundred times on the last one. The muscles are there.